How to Prepare Your Low-Voltage Business for a Sale or Exit in 2026: The 36-Month PE-Buyer Playbook

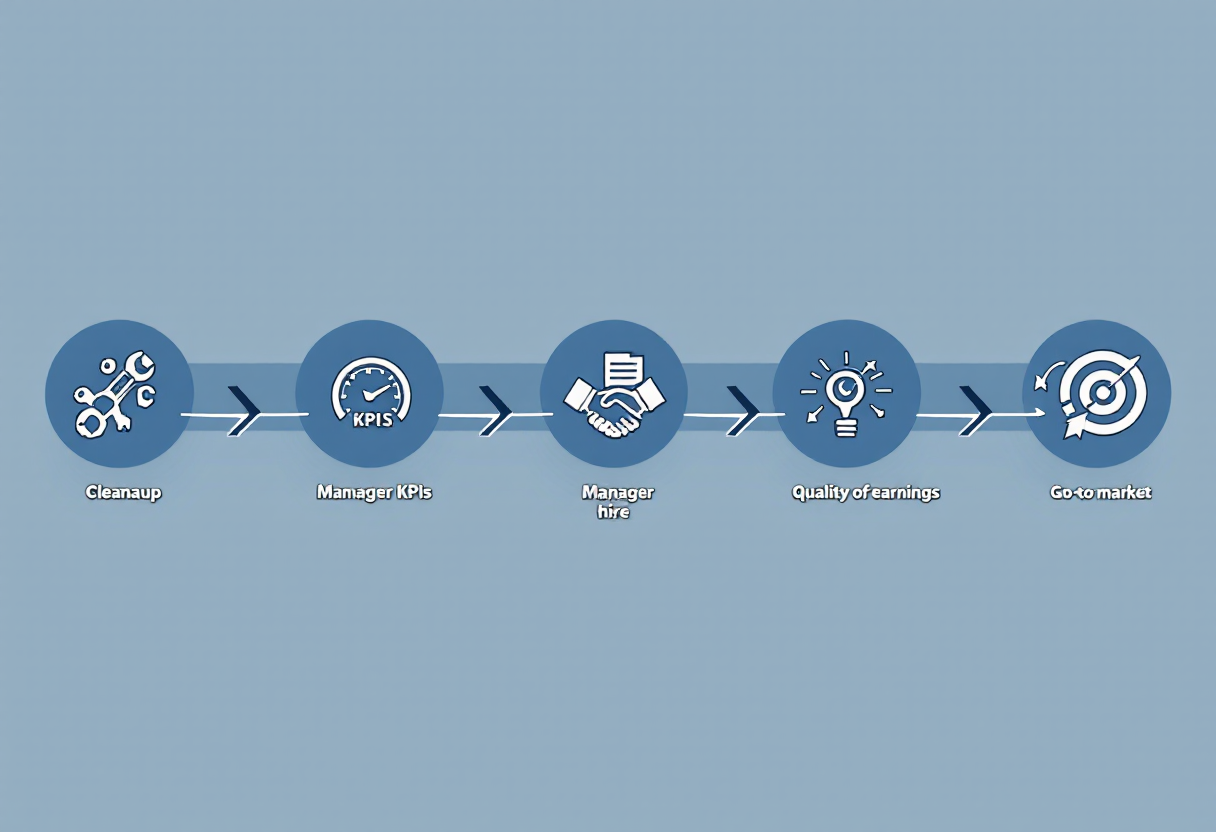

Preparing your low-voltage business for exit in 2026 works best as a 36-month process. The first 12 months tighten the operating story around recurring service revenue and structured cabling backlog, the middle 12 fix pre-LOI diligence gaps around technician certifications and license transferability, and the final 12 turn a single inbound offer into a competitive process with real bargaining power.

Exiting your low-voltage business is the single largest financial event most owners will ever face. This guide is the no-fluff playbook for low-voltage business owners who are 12-36 months from sale, covering how PE-backed buyers actually value your business in 2026, the 12 levers that move your multiple, pre-LOI diligence, deal-killers to fix before going to market, and the full 36-month exit prep timeline.

Buy-side M&A across 76+ active capital partners · Low-voltage M&A: AV, security, fire alarm, data cabling · Updated June 5, 2026

Most low-voltage owners decide to sell, hire a broker, and find out 90 days later that their business is worth 30% to 50% less than they thought. The owners who get the top-quartile price start preparing 24 to 36 months before they ever talk to a buyer. This guide is the 36-month playbook for how to prepare your low-voltage business for a sale or exit. It covers what private equity actually buys in structured cabling, fiber, AV, and data-center cabling; the 12 levers that move multiples; the documents PE will ask for before they send an indication of interest; and the deal-killers that re-trade low-voltage transactions during confirmatory diligence. Every number cites its source. Every recommendation comes from how the most active 2026 buyers behave.

If you are 6 to 36 months from a possible exit, this is the work that turns a 6x EBITDA outcome into a 10x EBITDA outcome. On a $3M EBITDA low-voltage business with data-center exposure, that is the difference between an $18M sale and a $30M sale. Whether you want to prepare your low-voltage business for a sale to private equity, prepare your low-voltage business for an exit to a strategic acquirer like Quanta, Dycom, or Comfort Systems, or simply maximize value over the next 1 to 3 years before going to market, the work below applies.

Building toward an exit in 12 to 36 months?

CT Acquisitions runs sell-side advisory for low-voltage owners $1M+ EBITDA across structured cabling, data-center cabling, fiber OSP, and AV integration. We also have operations specialists in our partner network who run pre-sale optimization engagements when the timeline is longer. Buyers pay our fee, not you.

What Private Equity Actually Buys in Low-Voltage (2026)

Multiple at a Glance · 2026

Low-Voltage Business Sale Multiples · 2026

EBITDA multiples by operator scale and RMR mix.

Source: CT Acquisitions analysis of low-voltage M&A (security, fire alarm, AV, data cabling). Recurring monitoring revenue drives 1-2 turns of EBITDA premium.

Related Cluster GuideAdjacent low-voltage/specialty-services vertical: see our companion guide on selling a fire protection business.

The AI data-center buildout is the single biggest demand event in the history of US specialty electrical and low-voltage contracting. Hyperscale capex from AWS, Microsoft, Google, Meta, and Oracle drove an estimated $300B+ in committed data-center spend across 2025 to 2026 (multi-source: company guidance from Q4 2025 earnings calls; Dell’Oro Group data-center capex tracker, January 2026). The US data-center structured cabling market alone was valued at $14.22B in 2024 and is forecast to roughly double to $28.34B by 2032 at a 9.1% CAGR (Data Bridge Market Research, “Global Data Center Structured Cabling Market”, 2025). Layer in the BEAD program (Broadband Equity, Access, and Deployment), which has allocated $42.45B across all 50 states with most state final proposals approved by NTIA across 2025, and the shovel-ready outside-plant fiber work loading into 2026 to 2028 is enormous (NTIA BEAD state allocation tracker, May 2026).

The sponsor money flowing in is not random. PE buys specific profiles, and the profile you build determines the multiple you get.

The PE-attractive low-voltage profile

- EBITDA threshold for a platform-quality deal: $1M to $3M is the entry band where sponsor-backed platforms run a competitive process. Below that, you are an add-on inside a roll-up. Above $5M, you are an attractive bolt-on for the larger commercial and mission-critical platforms. Above $15M, you are a platform candidate yourself.

- Service mix: 80%+ commercial is the line that separates premium pricing from generic. Residential structured wiring and smart-home AV cap the multiple at 2x to 4x SDE. Commercial structured cabling with healthcare, higher-ed, K-12, government, or mission-critical mix lifts the multiple into the 6x to 9x EBITDA band.

- Data-center exposure: 25% to 50% of revenue from hyperscaler (AWS, Azure, Google Cloud, Meta, Oracle) or top-tier colocation (Equinix, Digital Realty, QTS, CyrusOne, Switch) with at least one named-customer MSA is the single biggest premium driver. It can add 1.5x to 3x of EBITDA multiple on its own (estimate, calibrated against the Comfort Systems Oct 2025 8-K disclosure of 10x to 13x on its electrical and technology pair).

- Workforce certifications: 2+ BICSI RCDDs (Registered Communications Distribution Designers), at least 1 DCDC (Data Center Design Consultant), and 30%+ of installers carrying BICSI INSTL1 or INSTL2 credentials. Manufacturer-partner certified-installer status with Panduit, CommScope/SYSTIMAX, Corning, Belden, Berk-Tek, or Leviton.

- Customer concentration: No customer above 25% of revenue. Hyperscaler revenue concentrated in one logo without change-of-control protection is a hard deal-killer.

- Workforce model: 80%+ W-2 for field production. The DOL 2024 Final Rule on independent contractor classification (29 CFR Part 795) restored the Economic Reality Test, and buyers run it on every 1099 in the last 3 years.

- Safety record: EMR under 0.85 for 3 consecutive years. For hyperscaler work, this is usually a hard gate, not a preference.

- Owner role: Owner is in management, not the sole RCDD, not the sole license qualifier, and not the personal relationship for the top 5 customers.

Active low-voltage PE platforms in 2026

The table below covers the most active sponsor-backed low-voltage platforms in the 2024 to 2026 cycle. This is who will see your teaser. Add-on counts are point-in-time. Sources include 26North and One Rock press releases (Sept and Nov 2024); Quanta Services investor releases (Jul 17, 2024) and Form 8-K filings on SEC EDGAR; Dycom Industries Form 8-K (Nov 2025); Blackstone press release (Aug 21, 2025); Loenbro / Kohlberg / Braemont press release (Dec 2025); PrivSource specialty contractor deal tracker (May 2026); and trade press from EC&M, tEDmag, and Cabling Installation & Maintenance.

| Platform | Sponsor | Profile | Typical add-on EBITDA |

|---|---|---|---|

| ArchKey Solutions | 26North (acquired from One Rock Capital, closed Nov 4, 2024) | First 26North PE deal; over $1B value per Bloomberg; 4,000+ employees designing electrical, technology, specialty systems; national | $3M to $25M |

| Loenbro | Kohlberg (majority, closed Dec 2025); Braemont retained minority from Feb 2024 | Acquired Revolution Industrial Jan 2025; positioned for data-center and mission-critical; Mountain West expanding national | $2M to $15M |

| ICS Holding | Stellex Capital | Data-center and mission-critical electrical and low-voltage; national | $2M to $10M |

| Prime Electric | Truelink Capital | Mission-critical commercial; data-center cabling and electrical; West Coast and Pacific NW | $3M to $15M |

| Cupertino Electric (Quanta segment) | Acquired by Quanta Services for $1.54B upfront + up to $200M earnout, closed Jul 17, 2024 | 6th largest US electrical contractor; 25+ years data-center experience; 20M+ sq ft installed; national with Bay Area HQ | $5M to $25M+ bolt-ons |

| Power Solutions (Dycom segment) | Acquired by Dycom Industries for ~$1.95B, announced Nov 2025 | Premier data-center electrical contractor; immediately accretive to Dycom EBITDA margin per Dycom 8-K; national | $5M+ |

| Salute Mission Critical | Cordillera Investment Partners | Data-center commissioning and operations; aggressive add-on cadence; national data-center | $1M to $10M |

| Shermco Industries | Blackstone Energy Transition Partners (announced Aug 21, 2025 at ~$1.6B from Gryphon Investors) | 600+ NETA-certified technicians; data-center, utility, industrial electrical testing and commissioning; US and Canada | $2M to $15M bolt-ons |

| Pioneer Power Solutions Group | Multiple sponsors track | Active acquirer of mid-market commercial electrical with low-voltage divisions; regional | $1M to $8M |

| Mid-American Group | Industrial Opportunity Partners (and others per PrivSource) | Commercial and industrial electrical with structured cabling divisions; Midwest | $1M to $5M |

| InVio Communications | Allegiance Capital sponsor history (Tracxn-tracked roll-up activity) | Low-voltage AV and structured cabling integration; regional | $1M to $5M |

| Continental Wingate (data-center adjacent) | Multiple PE platforms in mission-critical services tracked by PrivSource | Hyperscaler-aligned design-build; national | $2M to $10M |

Estimate: at least 15 to 20 additional lower-middle-market sponsors are tracking the structured cabling and data-center cabling space as of mid-2026, with most still building their first platform. Sellers in the $1M to $5M EBITDA range should expect outreach from 5 to 10 different sponsors during a banker-run process.

Add to that list the strategic acquirers. Quanta Services (NYSE: PWR) closed Cupertino Electric in July 2024 at ~$1.54B upfront plus a $200M earnout, implying roughly 9x to 10x EBITDA on full-year 2024 EBITDA guidance of $155M to $175M (Quanta press release Jul 17, 2024; SEC EDGAR Form 8-K). Dycom Industries (NYSE: DY) announced the Power Solutions acquisition in Nov 2025 at ~$1.95B and also acquired Black & Veatch’s public carrier wireless telecommunications business in Q3 2025 (Dycom Form 8-K, SEC EDGAR). MasTec Communications (NYSE: MTZ) reported $3.4B trailing-12-month communications-segment revenue through Q4 2025 with double-digit growth driven by hyperscaler fiber and wireless densification (MasTec Q4 2025 earnings, Feb 2026). EMCOR Group (NYSE: EME) disclosed 5 acquisitions in 2025 including electrical and low-voltage targets per 10-K and 8-K filings; its US Electrical Construction and Facilities Services segments grew over 20% YoY in 2025. Comfort Systems USA (NYSE: FIX) closed 5 acquisitions in 2025 including Feyen Zylstra Holdings (Western Michigan, an electrical and technology contractor with low-voltage capability) and Meisner Electric on Oct 1, 2025, the pair adding $200M of annualized revenue and $15M to $20M of incremental EBITDA, implying ~10x to 13x on combined target EBITDA (Comfort Systems Form 8-K, Oct 23, 2025). IES Holdings (NASDAQ: IESC), MYR Group (NASDAQ: MYRG), APi Group (NYSE: APG), and Sterling Infrastructure (NASDAQ: STRL) round out the public-strategic buyer set. Estimate: 60 to 90 announced low-voltage contractor M&A transactions in 2025 across structured cabling, data-center cabling, fiber OSP, and AV/security-integration adjacencies, up from 40 to 60 in 2024 (composite of PrivSource, S&P Global Market Intelligence, and trade press).

Low-Voltage Valuation Multiples in 2026 (What You Are Actually Worth)

The multiple a buyer pays comes down to your size, your service mix, your data-center exposure, your workforce credentials, and your geographic footprint. Here is the 2026 range, cross-referenced from IBBA Market Pulse Q4 2025, BizBuySell Q3 2025 Insight Report, Capstone Partners Engineering & Construction M&A updates, and the disclosed strategic transactions cited above.

SDE multiples (smaller, owner-operated)

| SDE band | SDE multiple | Profile fit |

|---|---|---|

| Under $500K SDE | 2.0x to 3.0x | IBBA Market Pulse Q4 2025; BizBuySell Q3 2025 (specialty trades blended) |

| $500K to $1M SDE | 2.5x to 3.5x | IBBA Market Pulse Q4 2025; broker survey averages |

| Residential or one-off project mix only | 2.0x to 3.0x | Estimate; light recurring revenue caps the multiple |

| Commercial recurring or service-agreement mix 30%+ | 3.5x to 4.5x | Estimate; mirrors HVAC and security-integration premiums for recurring revenue |

EBITDA multiples (PE-attractive size)

| EBITDA band | Generic commercial structured cabling | Data-center specialty (hyperscaler / colo / mission-critical) | Fiber OSP / outside-plant telecom |

|---|---|---|---|

| $1M to $3M EBITDA | 5x to 7x | 7x to 9x | 4x to 6x |

| $3M to $5M EBITDA | 6x to 8x | 8x to 11x | 6x to 9x |

| $5M to $15M EBITDA | 7x to 10x | 9x to 12x | 6x to 9x |

| $15M+ EBITDA | 8x to 11x | 10x to 13x | 8x to 11x (with hyperscaler or carrier MSA) |

Generic commercial bands are estimates aligned with Capstone Partners Engineering & Construction M&A updates (2025) and the Comfort Systems Oct 2025 8-K disclosed bolt-on range. The data-center premium reflects the demand gap between PE platforms and qualified contractors and is supported by the Cupertino Electric implied 9x to 10x (Quanta, July 2024), the Power Solutions Dycom transaction (Nov 2025), the Shermco / Blackstone disclosed mid-teens multiple (Aug 2025), and the ArchKey / 26North $1B+ deal value (Nov 2024). Fiber OSP bands reflect the project-based nature of BEAD work; the high end requires a hyperscaler or Tier-1 carrier MSA in place.

Recent disclosed low-voltage and electrical transactions (2024 to 2026)

| Acquirer | Target | Date | Value | Implied multiple |

|---|---|---|---|---|

| Quanta Services | Cupertino Electric | Jul 17, 2024 | ~$1.54B upfront + $200M earnout | ~9x to 10x EBITDA (Quanta 8-K, SEC EDGAR) |

| 26North | ArchKey Solutions | Nov 4, 2024 | Over $1B per Bloomberg | Not officially disclosed; estimated low-double-digit EBITDA multiple |

| Blackstone Energy Transition Partners | Shermco Industries | Aug 21, 2025 | ~$1.6B from Gryphon Investors | Mid-teens EBITDA multiple (estimate, Blackstone press release) |

| Dycom Industries | Power Solutions | Announced Nov 2025 | ~$1.95B | Immediately accretive to Dycom EBITDA margin (Dycom 8-K) |

| Comfort Systems USA | Feyen Zylstra + Meisner Electric (pair) | Oct 1, 2025 | $200M revenue / $15M to $20M EBITDA contribution | ~10x to 13x (Comfort Systems Form 8-K Oct 23, 2025) |

| Kohlberg (majority) | Loenbro (Braemont retained minority) | Dec 2025 | Not disclosed | Not disclosed (Harris Williams transaction page) |

Sources: Quanta press release Jul 17, 2024 and SEC EDGAR Form 8-K; 26North and One Rock Capital press releases Sept and Nov 2024; Bloomberg ArchKey coverage Sept 2024; Blackstone press release Aug 21, 2025; Dycom Industries Form 8-K Nov 2025; Comfort Systems USA Form 8-K Oct 23, 2025; Loenbro / Kohlberg / Braemont joint press release Dec 2025.

The 12 Value Levers That Move Your Multiple (Ranked by Impact)

These are the levers that move low-voltage multiples in the 24 months before a sale. Each lever has a current state, a target state, an estimated financial impact, and a how-to. Ordering is by dollar impact per unit of effort, calibrated against PE deal commentary and the public-strategic 8-K filings referenced above. Each impact figure is an estimate unless tied to a named disclosed transaction.

Lever 1: Build data-center and hyperscaler revenue mix

Current: 0% to 10% of revenue from hyperscaler (AWS, Microsoft Azure, Google Cloud, Meta, Oracle Cloud) or top-tier colocation (Equinix, Digital Realty, QTS, CyrusOne, Switch). Most revenue is commercial new-construction and tenant fit-out. Target: 25% to 50% of revenue from data-center, with at least one named-customer MSA and a track record of 3+ completed projects per top customer. Impact: Estimate 1.5x to 3x EBITDA multiple uplift. This is the single biggest valuation lever in low-voltage in 2026. Comfort Systems disclosed 10x to 13x on its Oct 2025 electrical and technology pair, against 6x to 8x typical for generic commercial. How: Build a dedicated mission-critical practice. Hire a project executive with hyperscaler relationships. Subcontract under a Tier-1 EPC for your first 2 to 3 jobs to build the resume; then bid direct.

Lever 2: Get on a hyperscaler or cloud certified-partner program

Current: No direct hyperscaler vendor enrollment; the contractor is a sub of a Tier-1 general or EPC. Target: Approved or certified on at least one hyperscaler vendor program (AWS Partner Network, Microsoft Azure Cloud Adoption Framework partners, Google Cloud Partner Network, Meta facilities vendor list). For colo, certified on at least one of Equinix’s preferred-contractor lists. Impact: Estimate 0.5x to 1x EBITDA multiple uplift, and creates a defensible moat that survives founder transition. How: Assign an internal owner to the partner-application process 12 to 18 months pre-sale. Most programs require 2 to 3 reference customers, an EMR record, an insurance package, and a cybersecurity attestation.

Lever 3: Deepen fiber-optic specialty capability

Current: General structured cabling shop that pulls some fiber but does not own fusion splicers, OTDRs, or have dedicated splicing crews. Target: 3+ certified fiber splicing crews with current Sumitomo or Fujikura training certificates, multiple Fluke OTDR units with calibration records, documented MPO/MTP testing capability, and at least one in-house OSP design engineer. Impact: Estimate 0.5x to 1x EBITDA multiple uplift; opens up BEAD and hyperscaler fiber tail-circuit work that generic cabling shops cannot bid. How: Budget $150K to $400K for splicers and OTDR equipment with calibration cycle. Pay for crew training. Document splice loss results on every project as a quality artifact for the data room.

Lever 4: Build BICSI certification depth

Current: 1 RCDD on staff (often the founder), no DCDC, no TECH or INSTL2 documented for installers. Target: 2+ RCDDs, 1+ DCDC, RTPM project managers, and at least 30% of installers carrying BICSI INSTL1 or INSTL2 credentials. RCDD is the design-level cert; DCDC is data-center specific (BICSI certification pages, 2025). Impact: Estimate 0.5x to 1.5x EBITDA multiple uplift. RCDD depth separates a cable installer from a design-build firm in buyers’ eyes and is a gate for DoD and government projects. How: Pay for 2 to 3 staff to earn RCDD over 18 to 24 months. RCDD requires 2 years documented ICT design experience plus a current BICSI TECH, RTPM, DCDC, or OSP cert. Budget $5K to $10K per staff member.

Lever 5: Earn manufacturer-partner certified-installer status

Current: Distributor relationships only, ad-hoc product specification. Target: Certified installer status with at least 3 of the following: Panduit Certified PartnerAlliance, CommScope SYSTIMAX or NETCONNECT, Corning CCNT (Corning Certified Network Technician), Belden Certified System Vendor, Berk-Tek/Nexans LANmark, Leviton Atlas-X1, Hubbell NextSpeed. Documented training current and warranty-extension capability (typical 25-year manufacturer warranty pass-through). Impact: Estimate 0.5x to 1x EBITDA multiple uplift. Buyers value the warranty pass-through and the implied design discipline. Watch out: many partner agreements have change-of-control provisions that need to be confirmed pre-LOI. How: Pick 3 manufacturers aligned with your customer base. Apply for the program. Pay for training. Track active certifications in a shared compliance log.

Lever 6: Shift the mix from residential to commercial

Current: Predominantly residential structured wiring, smart-home AV, and one-off small commercial pulls. Target: 80%+ commercial; ideally a mix of healthcare, higher-ed, K-12, government, and mission-critical. Residential mix under 20% unless it is part of a builder-tier production program. Impact: Estimate 1x to 2x EBITDA multiple uplift. Buyers pay for repeatable commercial revenue and contract size, not one-off residential. How: Hire a commercial-focused estimator and project executive. Build pre-qualifications with 5 to 10 commercial GCs in your region. Drop residential work that does not fit the new ICP.

Lever 7: Cross-sell into AV, security, and access control

Current: Cable-pull only with no resale of AV equipment, IP cameras, access control, or wireless infrastructure. Target: Vertically integrated commercial integrator capable of design-build of structured cabling plus AV (Crestron, Extron, Q-SYS, Biamp dealer status), security (Genetec, Milestone, Avigilon, Verkada partner), and access control (HID, LenelS2, Brivo, Kisi). Impact: Estimate 1x to 1.5x EBITDA multiple uplift, and lifts revenue per project by 30% to 60%. How: Apply for 1 dealer relationship per category. Train 2 to 3 techs per system. Bundle into commercial bids by default. The security-integration adjacency has its own PE roll-up dynamics that are worth a separate conversation.

Lever 8: Build recurring service revenue (MAC contracts, MSA-based service)

Current: 100% project revenue; no service contracts. Target: 15% to 25% of revenue from MACs (moves, adds, changes), test-and-tone service, structured cabling maintenance contracts, fiber-cut emergency response retainers, and IoT maintenance. Impact: Estimate 0.5x to 1.5x EBITDA multiple uplift. Recurring revenue is what gets the multiple from 7x to 9x or higher. Buyers count recurring at a higher multiple than project revenue. How: Build a small dedicated service team. Sell annual MSAs to top-20 customers. Offer 24/7 fiber-cut response as a retainer. Track the recurring book separately in the financials.

Lever 9: Build the field software stack and operational maturity

Current: QuickBooks, spreadsheets, paper job folders, no formal project management software, no field-time capture system. Target: Procore or Autodesk Construction Cloud for project management; ServiceTrade or BuildOps for service-revenue tracking; ConnectWise PSA or Autotask if there is an MSP-adjacent business; BST10 or Foundation for industry-specific job cost; Fluke LinkWare Live for cable-cert deliverables; field-time and GPS via ClockShark or BusyBusy. Impact: Estimate 0.5x to 1x EBITDA multiple uplift, and the bigger benefit is that QoE adjustments drop sharply when the data is clean. How: Implement 18+ months pre-sale. Force tech adoption by tying payroll to job-completion data in the system. Run a parallel monthly close in the new system for 6 months before cutting over.

Lever 10: Convert to a W-2 workforce and clean up compliance hygiene

Current: Mixed 1099 and W-2; significant 1099 use for installers; missing I-9s on legacy staff; no documented background-check policy. Target: 80%+ W-2 for field production; all 1099 contracts limited to subs with their own GL/WC and EIN; clean I-9s in E-Verify for all hires from 2020 onward; documented drug-screen and background-check policy. Impact: Estimate 0.5x to 2x EBITDA multiple. At the high end, this is often the difference between deal-on and deal-off. The DOL 2024 Final Rule on independent contractor classification (29 CFR Part 795) was upheld through 2025 and remains the controlling test for misclassification. How: Convert all production roles to W-2 12+ months before going to market. Book the EBITDA hit and let it season. Buyers will normalize back to the W-2 cost anyway.

Lever 11: Expand the multi-state license portfolio

Current: One state license, founder is the sole qualifying party. Target: 3 to 5 state licenses held by named employees (not just the founder), with documented succession in case of qualifier departure. Specifically: California C-7 (low voltage) plus ACO (alarm) where applicable; Texas TDLR ES plus DPS where applicable; Florida ES (specialty electrical); and New York jurisdiction-by-jurisdiction with NYC DOB Master Electrician or equivalent for low-voltage portions. Impact: Estimate 0.5x to 1x EBITDA multiple uplift, and removes the key-man discount buyers would otherwise apply. How: Identify 2 to 3 RME (Responsible Managing Employee) or RMO (Responsible Managing Officer) candidates internally. Sponsor their exam prep. File qualifier changes 18 to 24 months pre-close.

Lever 12: Tighten the safety record and drop EMR under 0.85

Current: EMR around 1.0; OSHA 300 log shows recordable injuries; no documented confined-space or fall-protection program despite working at heights and in cable trays. Target: EMR under 0.85 for 3 consecutive years; written safety program; OSHA 30-Hour for all supervisors; documented confined-space, fall-protection, and electrical-safe-work-practices programs; safety committee meeting minutes; documented near-miss reporting. Impact: Estimate 0.5x to 1x EBITDA multiple uplift. For hyperscaler work, an EMR under 0.85 is often a hard gate, not a preference. How: Hire a part-time safety director if you do not have one. Write and train the OSHA Subpart M (fall protection) and 1910.146 (permit-required confined spaces) programs. Make EMR a board-level KPI.

Want to grow your business to maximize value before exiting?

We connect low-voltage owners with operations experts in our partner network who run 12 to 24 month pre-sale optimization engagements. The engagement pays for itself in incremental sale price.

What PE Asks Before They Send an LOI (The Pre-LOI Diligence Stack)

Before a PE firm or strategic acquirer commits to a letter of intent, they ask for a focused diligence package. The list below is what sophisticated buyers ask for in low-voltage today. The “why” and “how to prepare” expand each item to what is typical across the industry.

1. Three years of P&L by service line

Why PE asks: They are building the LTM EBITDA they will multiply, and they need to see the contribution mix from structured cabling, fiber OSP, AV integration, security, and service. Buyers value each service line at a different multiple, so the blend matters as much as the headline number.

How to prepare: Accrual-basis P&L by month, by service line, mapped to a clean chart of accounts. Reconcile to tax returns so there are no surprises in confirmatory. Tag every job with its primary service line in your job-cost system.

2. Customer concentration table (top 20 by revenue)

Why PE asks: Customer concentration is the single most common deal re-trade in low-voltage. Buyers want top 20 customers by revenue, percent of total, contract type (MSA vs. PO vs. T&M), MSA term, and renewal date. Hyperscaler concentration is a special case because of change-of-control review.

How to prepare: Build a customer concentration dashboard that refreshes monthly. Pre-disclose hyperscaler customers as “Top 5 Hyperscale Cloud Provider, NDA-protected, A++ credit profile, MSA active since 2021” rather than naming them; hyperscalers contractually prohibit naming them in marketing or M&A processes.

3. Backlog and pipeline by stage

Why PE asks: A real backlog supports the forward case. Buyers split backlog into verbal, awarded not started, in-progress, and billed not collected. Verbal-only awards get a haircut in QoE; awarded contracts with signed change orders do not.

How to prepare: Maintain a backlog tracker in your PM system. Include award date, contract value, percent complete, expected billing schedule, and customer name. Tie the in-progress balance to your percent-of-completion accounting.

4. Workforce summary

Why PE asks: Headcount, W-2 vs. 1099 split, BICSI cert counts (RCDD, DCDC, TECH, INSTL2), and manufacturer cert counts. Labor is the binding constraint in low-voltage, so the depth and credential mix of your workforce is a defensible asset. The 1099 mix also flags misclassification exposure.

How to prepare: Roster columns: role, hire date, full-time vs. part-time, W-2 vs. 1099 (with classification rationale), comp structure, BICSI certifications held with expiration date, manufacturer certifications held, OSHA 10/30 status, and any active non-compete or non-solicit. Calculate 12-month rolling installer retention.

5. Geographic and license footprint

Why PE asks: Which states, counties, and municipal jurisdictions does the company hold low-voltage and electrical licenses in, and who is the named qualifier on each? This gates the buyer’s ability to operate the company on day one post-close.

How to prepare: Spreadsheet by state and jurisdiction: license type, license number, named qualifier (RME / RMO / master electrician), expiration date, renewal cycle, and any open compliance items. Flag any license where the founder is the sole qualifier.

6. Manufacturer-partner certified-installer status

Why PE asks: Panduit, CommScope, Corning, Belden, and others have change-of-control provisions in their certified-installer agreements that can terminate or require re-approval on a sale. Losing certified status disqualifies the buyer from extending the manufacturer warranty, which is the entire point of certified installation.

How to prepare: Inventory all manufacturer-partner agreements. Read the change-of-control language on each one. Pre-clear the deal with each manufacturer 6 to 12 months pre-close under NDA.

7. Customer change-of-control consent matrix

Why PE asks: Each top-20 customer MSA either requires written consent on CoC, written notice, or neither. The matrix tells the buyer which customers might walk and how much friction the post-close consent process will create.

How to prepare: Read every top-20 customer MSA. Build the matrix. For any “written consent required” customers, pre-clear under NDA 6 to 12 months pre-close.

8. Recent change-of-control language samples from MSAs

Why PE asks: Buyers want to read the actual CoC clauses, not the seller’s summary. This is often the gating item for the deal.

How to prepare: Redact and prepare 5 to 10 representative customer MSAs for the data room, with CoC clauses highlighted.

9. Quality of Earnings or audited financials

Why PE asks: Sophisticated buyers expect a sell-side QoE for deals at $2M+ EBITDA. If you do not have one, they will build their own and use the findings to negotiate the price down.

How to prepare: Commission a sell-side QoE at T-9 to T-7 months. Cost: $50K to $150K typical for a $1M to $5M EBITDA target. See the dedicated QoE section below.

10. Add-back estimates

Why PE asks: They want a sneak peek at your adjusted EBITDA story before they sink diligence cost into the file. Aggressive or undocumented add-backs discount the rest of your numbers.

How to prepare: Build a bridge from book EBITDA to adjusted EBITDA, line by line. Document every add-back with the underlying invoice or payroll record. Common low-voltage add-backs: owner compensation above market, personal vehicles and travel, one-time legal or settlement costs, discontinued service lines or one-off project losses, family members on payroll above market comp, excess rent on owned real estate at related-party rates, and one-time COVID-era costs.

Confirmatory Diligence (After You Sign the LOI)

Once an LOI is signed and exclusivity starts (typically 60 to 120 days in low-voltage because of the commercial and mission-critical contract review), the buyer runs parallel workstreams. This is the depth of inspection your business will undergo. If anything was hiding, it surfaces here.

- Quality of Earnings (QoE). Outside accounting firm runs percent-of-completion revenue recognition testing, job-cost detail review on the largest 20 jobs in the trailing 24 months, working capital normalization (low-voltage WC requirement is typically 8% to 12% of revenue), backlog haircut for verbal-only awards, and add-back validation. Buyer’s QoE cost: $75K to $300K typical for $2M to $10M EBITDA low-voltage. Output: an adjusted EBITDA number the buyer locks into the model.

- Customer interviews. Calls with top 10 to 15 accounts (always with seller pre-clearance), MSA review (assignment clauses, change-of-control triggers, renewal dates), and reference checks on technical performance and on-time delivery.

- Workforce review. I-9s, background checks, drug screens, certification records, union vs. open-shop status, prevailing-wage compliance for any public projects, and 1099 worker classification review under the DOL Economic Reality Test (29 CFR Part 795).

- Safety and OSHA review. OSHA 300 logs for the last 3 years, EMR letters from carriers, written safety program review, confined-space and fall-protection program audit, and incident history.

- IT and cybersecurity review. Standard for any contractor with hyperscaler exposure. MFA on all systems, EDR coverage, documented incident response, vendor risk management, and any prior incident remediation. Hyperscalers and large colos increasingly require SOC 2 Type II, ISO 27001, or NIST CSF compliance.

- Insurance review. GL, auto, umbrella, professional / E&O for design-build, workers’ comp, cyber liability, and builders risk. Bond capacity verification from the surety.

- Real-estate and equipment lease review. Cable reels, splicing trucks, OTDR equipment, lift trucks, and operating lease vs. capital lease classification. Phase I ESA on any owned property where the company also operates.

- IP and software license review. Custom-developed cable management or PM tools, Fluke LinkWare licenses, Visio templates, and any third-party software at risk on CoC.

- Tax review. Federal income tax, state sales / use tax (cable products are taxable in most jurisdictions, and under-collection of use tax is common in multi-state contractors), and payroll tax.

- Customer change-of-control consent matrix. Track which MSAs require written consent vs. notice vs. neither. Begin securing consents in parallel with confirmatory diligence so the close is not gated.

Why You Should Pay for Your Own Quality of Earnings Before Going to Market

A sell-side QoE is your own outside accountant’s QoE, paid for by you, before you go to market. It does three things in low-voltage: it pre-empts the buyer’s QoE by getting to the adjusted EBITDA number first with documentation; it surfaces percent-of-completion and job-cost issues you can fix before the buyer sees them; and it tightens the EBITDA number you take to market, which directly drives the headline price. Buyers in low-voltage have been burned repeatedly on percent-of-completion revenue recognition on long-duration projects (typical structured cabling project is 90 to 270 days; large data-center buildouts can run 12 to 24 months), job-cost mis-coding, and backlog inflation. Walking into a process with a pre-sell QoE from a credible firm signals operational maturity and protects you from buy-side adjustments that wipe out 0.5x to 1.5x of multiple. The full list of low cost franchise opportunities covers the active buyers, fee structures, and unit-economics for each.

Cost

- $50K to $150K for sell-side QoE on a $1M to $5M EBITDA low-voltage target, scaling with complexity (multiple entities, multi-state, messy job-cost detail).

- Firms commonly engaged in low-voltage QoE (no endorsement): Bennett Thrasher, BPM (formerly Burr Pilger Mayer), BDO USA, Cherry Bekaert, CohnReznick, CrossCountry Consulting, Eisner Advisory, Grant Thornton, Marcum, Riveron, RubinBrown, and Withum.

- Timing: commission at T-9 to T-6 months from going to market. Earlier than that and the trailing 12-month financials are stale by close. Later than that and there is no time to fix issues.

ROI

Common pattern across QoE provider content: on a $3M EBITDA low-voltage business, moving the multiple from 7x to 8x equals $3M of additional sale price. A $75K QoE investment that supports the 1x lift is a 40x return. Low-voltage specific example: a $4M revenue structured cabling business reported $900K EBITDA on tax returns; the sell-side QoE landed at $640K adjusted EBITDA after percent-of-completion correction and backlog haircut. The owner fixed the underlying accounting over the next 6 months and went to market at a clean $850K adjusted EBITDA the following year, with documentation that survived buy-side QoE without re-trade.

Deal-Killers That Re-Trade Low-Voltage Transactions (Avoid These)

These are the recurring kill-shots cited across low-voltage M&A advisory content and confirmatory diligence findings. Most are fixable in 12 to 24 months. None are fixable in 30 days.

1. State low-voltage license tied to a single person who is exiting

Most states require a qualifying party or qualifier for low-voltage work. California requires a C-7 contractor license held by a Responsible Managing Employee (RME) or Responsible Managing Officer (RMO); Texas requires TDLR ES plus DPS for alarm work; Florida requires ES specialty electrical license; New York runs city-by-city. If the founder is the sole qualifier and is exiting at close, the buyer cannot operate post-close. Fix: identify and license a successor RMO / RME 18 to 24 months pre-close, name them on the license, and let them carry projects.

2. BICSI RCDD concentration on the founder

Same dynamic as #1 but on the design side. If the founder is the sole RCDD, every design deliverable carries personal risk. Buyers will apply a key-man discount of 1x to 2x EBITDA. Fix: pay for 2 to 3 additional staff to earn RCDD over 18 to 24 months. RCDD requires 2 years documented ICT design experience plus a current BICSI TECH, RTPM, DCDC, or OSP cert (BICSI RCDD certification page, 2025).

3. Hyperscaler customer concentration without change-of-control protection

Hyperscalers run strict vendor approval and change-of-control reviews. A 50%+ concentration on one hyperscaler with a contract that allows them to walk on a CoC event is a deal-killer. Fix: pre-clear the deal with the customer 6 to 12 months pre-close under strict NDA. Build the procurement-team relationship so the CoC clause is treated as notice-only, not a re-approval gate. Diversify if pre-clearance is not possible.

4. Hyperscaler client list disclosure

Hyperscalers contractually prohibit naming them as customers in marketing or in M&A processes. Even in CIM materials, customer identities are usually disclosed as “Top 5 Hyperscale Cloud Provider, NDA-protected, A++ credit profile, MSA active since 2021”. Fix: build customer reference dossiers that buyers can review under clean-room protocols without the seller violating NDAs.

5. Manufacturer-partner certified-installer status with CoC clauses

Panduit, CommScope, Corning, Belden, and others have CoC provisions in their certified-installer agreements that can terminate or require re-approval on a change of ownership. Losing certified status disqualifies the buyer from extending the manufacturer warranty, which is the entire point of certified installation. Fix: pre-clear with each manufacturer partner. Most will reaffirm on close if the buyer has comparable certified-installer status; some will not.

6. W-2 vs. 1099 misclassification

The DOL 2024 Final Rule (29 CFR Part 795, effective March 11, 2024 and reaffirmed across 2025) restored the multi-factor Economic Reality Test for classifying workers as independent contractors. Buyers run this test on every 1099 in the contractor’s last 3 years. Common findings: 1099 used for production roles the company directs day-to-day; 1099 workers with no other clients; 1099 workers who use company-provided tools or vehicles; 1099 workers who have been with the company for years. Any of these will produce a buy-side reclassification reserve, typically $5K to $25K per worker per year of exposure, off the price. Fix: convert all production roles to W-2 12+ months before going to market.

7. Data-center customer cybersecurity requirements not met

Hyperscalers and large colos increasingly require contractors to maintain SOC 2 Type II, ISO 27001, or NIST CSF compliance. If the seller cannot show evidence of basic cybersecurity hygiene (MFA on all systems, EDR coverage, documented incident response, vendor risk management), the customer may not approve the CoC. Fix: stand up a basic cyber program 18+ months pre-close. Hire a vCISO or use a managed compliance partner.

8. Bond capacity and surety relationship

Many commercial and government projects require bid bonds, performance bonds, and payment bonds. If the seller’s surety relationship is collateralized by the founder’s personal guarantee, the buyer either has to assume the PG, post collateral, or re-bid the surety. Each is a friction point. Fix: build the surety relationship on the company balance sheet (not the founder’s), and increase aggregate capacity to 2x to 3x current backlog 12+ months pre-close.

9. OSHA confined-space and fall-protection program gaps

Low-voltage work involves cable trays, plenum spaces, telecom rooms, lift work in data halls, and on the fiber side bucket-truck and manhole / confined-space work. OSHA Subpart M (fall protection) and 1910.146 (permit-required confined spaces) are the high-risk standards. An open OSHA inspection, a recent serious or willful violation, or a recordable involving fall or confined-space exposure will spook buyers. Fix: documented written programs, training records, equipment inspection logs, and EMR under 0.85 for 3 years.

10. Cybersecurity insurance gap and incident history

Many low-voltage contractors have been hit by ransomware in 2023 to 2025. If the seller had an incident and the recovery is undocumented, or if there is no cyber policy in place at $1M+ limit, this is a real deal-friction point. Fix: buy a cyber policy at $5M aggregate with $5M per-incident limits. Document any prior incident and the remediation.

11. Related-party rent at non-market rates

Founders often own the building and rent it to the company at above-market or below-market rates. Either creates a QoE adjustment that flows directly to EBITDA. Buyers normalize to market rent. Fix: order an independent market-rent appraisal 6 to 12 months pre-close. Adjust the rent in the QoE add-backs and present the normalized number in the CIM.

12. The founder is the entire business-development function

The founder personally manages the top 5 customer relationships. There is no sales team, no estimator with customer-facing exposure, no project executive who attends pre-bid meetings. The buyer perceives that revenue evaporates on Day 1 post-close. Fix: hire or promote a VP of Sales / VP of Business Development 18 to 24 months pre-close. Transition customer relationships before the LOI. Document customer-facing roles and contact frequency.

The 36-Month Exit Prep Timeline

T-36 to T-24 months: Foundation phase

- Engage a CFO (fractional or full-time) if not in place. Get GAAP-quality monthly financials with percent-of-completion done correctly.

- Start the RCDD and DCDC certification track for 2 to 3 additional staff.

- Identify and license successor state-license qualifiers (RMO / RME).

- Convert 1099 production roles to W-2; book the EBITDA impact and let it season.

- Diversify the customer base; reduce top-5 concentration under 60% if currently higher.

- Implement Procore or Autodesk Construction Cloud for project management.

- Implement ServiceTrade or BuildOps for service-revenue tracking.

- Add a manufacturer-partner certification (Panduit, CommScope, Corning, Belden) if not already certified.

- Begin building data-center revenue if generic commercial today.

T-24 to T-18 months: Hygiene phase

- Hire or promote a VP of Sales / VP of Business Development.

- Document customer-facing roles below the founder for the top 10 accounts.

- Stand up a written safety program; target EMR under 0.85.

- Begin SOC 2 Type II or NIST CSF readiness work.

- Renegotiate the surety relationship to balance-sheet collateral, not founder personal guarantee.

- Begin engaging M&A advisor finalists (interview 4 to 6 bankers; pick 1 to 2 to lock in at T-12).

- Order an independent market-rent appraisal if real estate is held by a related party.

T-18 to T-12 months: Prep phase

- Lock in an M&A advisor (boutique investment bank specializing in specialty contracting and engineering services; typical fee 1% to 4% of TEV plus retainer).

- Commission the sell-side QoE (provider engaged at T-9, fieldwork starts T-7).

- Start documenting all add-backs and one-time items with supporting evidence.

- Begin pre-clearing manufacturer-partner CoC with Panduit, CommScope, Corning, Belden.

- Begin pre-clearing top-3 customer CoC under strict NDA.

- Lock in 3 years of audited or reviewed financials if not already audited.

T-12 to T-6 months: Marketing prep phase

- QoE field work T-9 to T-7; final deliverable T-6.

- Prepare the CIM (Confidential Information Memorandum) with the advisor.

- Build the data room (virtual, with logical folder structure: financials, customers, contracts, employees, licenses, real estate, IP, insurance, tax, litigation).

- Build the buyer list with the advisor: typically 30 to 80 strategic plus PE buyers.

- Stress-test the management presentation.

- Identify and remediate any remaining deal-killers.

- Update org-chart documentation showing decision rights and customer relationships.

T-6 to T-3 months: Process phase

- Drop the CIM and teaser to the buyer list.

- Receive Indications of Interest (IOIs) at T-5 to T-4.

- Down-select to 8 to 12 buyers for management presentations.

- Conduct management presentations T-4 to T-3.

- Receive LOIs at T-3; down-select to 1 to 2 buyers for confirmatory diligence.

T-3 to Close: Closing phase

- Confirmatory diligence weeks 1 to 8.

- Definitive agreement drafting weeks 4 to 10.

- Final regulatory and consent items weeks 8 to 12.

- Close.

End-to-end from advisor engagement to close in a well-run low-voltage process: 9 to 14 months. From the day you decide to sell to the optimal close: plan 24 to 36 months of operational prep first.

Frequently Asked Questions

What is my low-voltage business worth in 2026?

For generic commercial structured cabling at $1M to $3M EBITDA, expect 5x to 7x. For data-center specialty with hyperscaler exposure at $3M to $5M EBITDA, expect 8x to 11x. For fiber OSP work, especially BEAD-driven, expect 4x to 9x because of the project-based nature and thin maintenance tails. Premium drivers that stack on top include BICSI RCDD depth, manufacturer-partner certified-installer status, W-2 workforce, EMR under 0.85, and a multi-state license portfolio held by named employees (not just the founder).

Who is buying low-voltage contractors right now?

Strategic acquirers including Quanta Services, Dycom, MasTec, EMCOR, Comfort Systems USA, IES Holdings, MYR Group, APi Group, and Sterling Infrastructure, plus PE platforms including ArchKey (26North), Loenbro (Kohlberg with Braemont retained minority), Shermco (Blackstone Energy Transition Partners), ICS Holding (Stellex), Prime Electric (Truelink), Cupertino Electric (now a Quanta segment), Power Solutions (now a Dycom segment), and Salute Mission Critical (Cordillera). Estimate: at least 15 to 20 additional sponsors are scouting the structured cabling and data-center cabling space as of mid-2026.

How long does it take to sell a low-voltage business?

From advisor engagement to close in a well-run process, plan 9 to 14 months. From the day you decide to sell to the optimal close, plan 24 to 36 months of operational prep first. The minimum useful prep window is 12 months because most of the high-leverage levers (building data-center revenue, lifting BICSI RCDD count, converting 1099 to W-2, dropping EMR under 0.85, commissioning a sell-side QoE) need 12+ months of clean trailing-twelve-months data to be credible to a buyer.

Do I need a Quality of Earnings report before going to market?

For anything over $2M EBITDA, yes. A sell-side QoE typically costs $50K to $150K for a $1M to $5M EBITDA low-voltage target and protects 0.5x to 1.5x EBITDA from buy-side adjustments. Low-voltage QoE adjustments concentrate around percent-of-completion revenue recognition on long-duration projects (90 to 270 days for structured cabling, 12 to 24 months for large data-center buildouts), job-cost mis-coding, backlog inflation from verbal-only awards, and working capital normalization at the typical 8% to 12% of revenue band. Commissioning at T-9 to T-6 gives time to fix issues.

What kills low-voltage M&A deals at the LOI to close stage?

The top three are state-license qualifier risk (founder is the sole license-holder), customer-concentration in hyperscalers without change-of-control protection, and 1099 worker misclassification under the DOL 2024 Final Rule (29 CFR Part 795). Manufacturer-partner certified-installer CoC is a fast-rising fourth because Panduit, CommScope, Corning, and Belden agreements can terminate or require re-approval on a sale, and losing certified status disqualifies the buyer from the 25-year warranty pass-through.

How do I diversify away from hyperscaler concentration without losing my premium multiple?

Add 2 to 3 large colocation customers (Equinix, Digital Realty, QTS, CyrusOne, Switch), plus 2 to 3 healthcare-system anchors and 2 to 3 higher-ed anchors. The premium for data-center mix comes from depth of capability, not just hyperscaler logos, so colos count. Hyperscalers contractually prohibit naming them as customers in marketing or M&A processes, so the relationship value sits in the technical reference dossier you can show under clean-room protocols, not in the logo wall.

What to Do Next

The low-voltage owners who get the top-quartile multiple all do the same three things. They start preparing 24 to 36 months before they want to be out. They build BICSI RCDD depth, manufacturer-partner certified-installer status, and a W-2 workforce 12+ months pre-sale. And they invest in a sell-side QoE before any buyer sees a CIM.

If you are 12+ months from a potential exit and want a structured pre-sale optimization roadmap, CT Acquisitions has low-voltage operations specialists in our partner network who run multi-quarter prep engagements covering BICSI track design, hyperscaler partner enrollment, percent-of-completion accounting cleanup, and qualifier-license succession. If you are 6 to 12 months out and ready to start the sell-side process, our M&A advisory team runs the buyer outreach across the 27+ active PE platforms and the public-strategic buyer set (Quanta, Dycom, MasTec, EMCOR, Comfort Systems, IES, MYR, APi, Sterling).

Buyers pay our fee, not you. Either way, the first 30 minutes are free.

Ready to talk?

Schedule a 30-minute exit-readiness call

Or read more: Sell Your Security Integration Business (sibling vertical with AV / access-control overlap) | Talk to a CT Acquisitions advisor

Ready to Explore Your Options?

A 30-minute confidential conversation is all it takes.