How to Prepare Your Law Firm for a Sale or Exit (2026)

Updated April 2026 · CT Acquisitions

Most law firm partner-owners decide to sell, talk to a broker, and find out 90 days later that the deal they pictured is not legal in their state. Private equity cannot directly own a US law firm in 46 of 50 jurisdictions under ABA Model Rule 5.4. Only Arizona, Utah, Washington DC, and Puerto Rico permit direct non-lawyer equity. Everywhere else, capital has to flow through a Managed Services Organization (MSO) sitting next to a lawyer-owned firm. Owners who get the top-quartile price start preparing 24 to 36 months before they ever talk to a buyer, and they build their books, their financials, and their structure around the rules that actually govern the deal. This guide is the 36-month playbook for that work. It covers what private equity actually buys in legal services, the 14 levers that move multiples, the documents PE asks for before sending an indication of interest, and the deal-killers that re-trade law firm transactions in confirmatory diligence. Every number cites its source.

If you are 6 to 36 months from a possible exit, this is the work that turns a 3x EBITDA outcome into a 5x EBITDA outcome on a transactional or business-law book, or a 3x outcome into a 7x to 10x outcome on a platform-tier plaintiff PI book. On a $2M EBITDA practice, that delta is the difference between a $6M sale and a $10M sale on the conservative path, and an $8M sale vs. a $20M sale on the PI path. Whether you want to prepare your law firm for a sale to private equity through an MSO or ABS structure, prepare your law firm for an exit to a strategic acquirer through lateral acquisition or full-firm merger, or simply maximize value over the next 1 to 3 years before going to market, the work below applies.

Building toward an exit in 12 to 36 months?

CT Acquisitions runs sell-side advisory for law firm partner-owners $1M+ EBITDA. We have legal-services operations specialists in our partner network who run pre-sale optimization engagements when the timeline is longer. Buyers pay our fee, not you.

What Private Equity Actually Buys in Law Firms (2026)

The legal sector sits much earlier in its PE entry than HVAC, dental, or accounting. Roughly a dozen PE-backed MSO deals closed in 2025, with Samson Partners Group tracking 10 in 2024 and projecting 20 in 2026, and approximately 70% of those deals concentrated in personal injury (Bloomberg Law, “Private Equity Woos Personal Injury Law Firms With Profits, Tech”, April 2026; Holland & Knight, October 2025). Arizona has approved 136 Alternative Business Structures as of April 30, 2025, with 59% of newly licensed 2024 ABSs wholly owned by non-lawyers and at least 15 entities tied to PE or litigation finance (Sidley Austin, November 2025; Bloomberg Law, May 2025). On top of that, six US law firm mergers in 2025 involved two firms each with 100+ partners, with another six announced for 2026 close (Altman Weil, 2025).

The PE-attractive law firm profile

- EBITDA threshold for a platform-quality deal: $1.5M to $5M EBITDA puts a firm in the active PE deal flow as a platform candidate for plaintiff PI, and as a tuck-in or bolt-in for transactional or boutique practices. Below $1M, you are typically an add-on or a lateral target. Above $10M EBITDA, you are an attractive platform candidate for sponsors building a national legal-services brand.

- Practice area: Plaintiff personal injury commands the strongest demand and the widest multiple range (small PI 3.0x to 5.0x, platform PI 7.0x to 10.0x+ EBITDA). Transactional and corporate boutiques typically trade on 0.87x to 1.5x revenue. Immigration, IP, ERISA, and tax boutiques with payroll-based or retainer-anchored recurring revenue trade in a 2.5x to 5.0x EBITDA band. Insurance defense, family, and criminal anchor the bottom of the practice-area ranking (CSuite Financial Partners, 2025; Peak Business Valuation, 2025; The Law Practice Exchange, 2025).

- Deal structure: Arizona ABS for full equity ownership, Utah sandbox for limited cases, or MSO + PLLC structure (anywhere in the US, validated by Texas Ethics Opinion 706 in February 2025). The MSO route is dominant in current US deal flow.

- Geography: Sun Belt, Texas, Florida, Arizona, Pennsylvania, Carolinas, and growth metros concentrate sponsor demand. Multi-state attorney bench through UBE-score transfer is a multiplier.

- Client or referral-source concentration: No single client above 10% of revenue. Top 5 clients below 30%. For PI, no marketing channel above 35% of signed cases. Owner-rainmaker book above 50% triggers earn-out structures or material price discount.

- Owner role: Managing attorney or COO in place 12+ months pre-sale. Owner is not the only rainmaker, not the only signatory, not the only relationship holder on top clients.

- Compliance posture: Clean IOLTA trust accounting, no open state bar disciplinary inquiries, no active malpractice claims, conflict-check policy documented, partnership agreement assignable.

Active law firm PE platforms and capital providers in 2026

The list below covers the most active sponsor-backed platforms, litigation funders, ABS firms, and strategic legal-services acquirers verifiable through press releases, sponsor sites, and trade press as of May 2026. The named PE-backed direct law firm list is materially shorter than HVAC and concentrated in personal injury and mass tort.

| Platform | Sponsor / Investor | Profile |

|---|---|---|

| Rafi Law Services (MSO) / Rafi Law Group | Fortress Investment Group | $125M investment April 2026; ~$450M MSO valuation; Arizona ABS plus MSO; 26 attorneys, ~250 support staff, seven Arizona offices; personal injury |

| Orion Legal (MSO) / Dudley DeBosier Injury Lawyers | Uplift Investors | Closed January 22, 2026; second add-on by May 2026; Louisiana MSO; plaintiff PI; fund targets $10M to $40M EBITDA platforms |

| Sbaiti & Co. (MSO) | Certum Group | Operating MSO serving multiple PI firms; mass tort and personal injury |

| Scout Law Group | 777 Partners (Miami) | Arizona ABS; personal injury and general civil; authorized post-2021 |

| Eudia Counsel | General Catalyst (Eudia raised $105M Series A in February 2025) | Arizona ABS approved June 2025; corporate, contracting, M&A diligence via AI and attorneys |

| KPMG Law US | KPMG LLP | Arizona ABS approved February 27, 2025; tax, trusts, estates, corporate compliance |

| Pravati Capital | Litigation funder | Multiple ABS structures since 2020; mass tort and contingent-fee plaintiff |

| Virage Capital Management | Litigation funder | Multiple ABS structures since 2020; mass tort and plaintiff |

| Burford Capital (NYSE: BUR) | Public litigation funder | Capital provider, not direct owner; $7.5B portfolio, $12.1B lifetime commitments at FY2025 close |

| Omni Bridgeway | Public Australian litigation funder | Capital provider; commercial litigation and class action; active US presence |

| Therium Capital Management | Private litigation funder | Capital provider; commercial litigation and class action; major US presence |

| Esquire Financial Holdings (NASDAQ: ESQ) | Public | Bank; case-cost financing for plaintiff PI; Piper Sandler 2025 Bank & Thrift Sm-All Stars |

| DWF Group (UK) | Inflexion Private Equity Partners | UK take-private October 2023 at £342M (~$420M USD); FY April 2025 revenue £466M (+8% YoY); 1,100 lawyers |

| Slater + Gordon (Australia) | Allegro Funds | Take-private April 2023 at A$78M (~$52M USD); personal injury and consumer |

| Tierra Capital Partners | Standalone PE | MSO via legal-services platform; targeting $100M to $125M fund per Bloomberg Law |

| Pine Valley Capital Partners | Standalone PE | MSO via legal-services platform; legal, financial, and allied services |

| Stifel Financial Corp. | Stifel | Strategic finance and MSO; legal-services advisory |

| Apollo Global Management | Apollo | MSO position via legal-services exposure; listed among investors mentioned in Bloomberg Law |

| Samson Partners Group | Standalone advisory and PE | MSO formation and brokerage; tracks ~20 MSO deals projected for 2026 |

| Aprio Legal | Aprio (PE-backed accounting platform) | ABS in formation; tax, transactional, and advisory; joined Private Equity Legal Alliance 2025 |

| Rocket Lawyer | VC-backed (private) | Arizona ABS approved; consumer legal |

| Onit | Stalwart Capital Partners (take-private 2025) | Strategic acquirer of legal tech; legal ops and contract lifecycle |

| LegalZoom (NASDAQ: LZ) | Public | Strategic acquirer of legal tech and adjacent services; consumer legal |

Add to that list the strategic acquirers running lateral-hire programs and full-firm mergers. McDermott Will & Schulte completed its mid-2025 combination at roughly $2.8B in combined 2024 revenue and confirmed in November 2025 that it is exploring outside investment (ABA Journal, “McDermott’s Private Equity Plan”, February 2026). Polsinelli PC posted $964M in 2024 revenue (+11.4% YoY) and added 133 net lawyers, including roughly 50 in a new Philadelphia office. Husch Blackwell LLP grew to $707.8M in 2024 revenue (+15.6% YoY) and added 126 lateral attorneys (Missouri Lawyers Media, June 2025). Fragomen, Del Rey, Bernsen & Loewy LLP is the dominant immigration acquirer at ~$850.9M revenue with three publicly disclosed acquisitions of immigration-tech firms (SimpleCitizen 2024; Nomadic earlier; Ramineni Law Associates April 2023). Lewis Brisbois Bisgaard & Smith LLP and Wilson Elser Moskowitz Edelman & Dicker LLP run insurance-defense lateral roll-ups; PE interest in Lewis Brisbois is trade-press rumored only as of May 2026 and no public deal has closed (flag: rumored, not confirmed). Alternative legal services providers such as UnitedLex and Axiom are the most likely strategic acquirers for legal-tech-adjacent boutiques in e-discovery, contract management, and managed legal services.

Law Firm Valuation Multiples in 2026 (What You Are Actually Worth)

The defining feature of law firm valuation is that practice area matters more than EBITDA size. Plaintiff personal injury commands the highest multiples because of contingent-fee revenue visibility and case-inventory predictability. Transactional and corporate law typically transact on revenue multiples rather than EBITDA, because partner compensation already absorbs market-rate owner pay. Insurance defense and other hourly-billing practices anchor toward the middle of the range. The ranges below cross-reference Peak Business Valuation, The Law Practice Exchange, CSuite Financial Partners, Abogados Now, LeanLaw, Arrowfish Consulting, and Eton Venture Services valuation guides for 2025 and 2026.

SDE multiples (smaller, owner-operated practices)

| Profile | SDE multiple | Source |

|---|---|---|

| Solo or two-attorney general practice | 1.0x to 2.0x | Peak Business Valuation 2025; Cotterman IADC valuation paper (2018, referenced 2025) |

| Owner-dependent practice with no documented systems | 1.5x to 2.5x | The Law Practice Exchange Dallas boutique data 2025 |

| Documented systems, cross-trained team, transferable referral sources | 2.44x to 2.84x | Peak Business Valuation 2025 |

| Specialty boutique (IP prosecution, ERISA, immigration with payroll-based recurring clients) | 2.5x to 4.0x | Peak Business Valuation 2025; LeanLaw 2025 |

EBITDA multiples by EBITDA band and practice area

| EBITDA band | General practice | PI / plaintiff | IP / tax / immigration / ERISA boutique | Insurance defense / family / criminal |

|---|---|---|---|---|

| Under $500K | 1.5x to 3.0x | 1.0x to 3.0x (book attrition risk) | 2.0x to 3.5x | 1.5x to 2.5x |

| $500K to $1M | 2.5x to 3.5x | 3.0x to 5.0x | 3.0x to 4.5x | 2.0x to 3.0x |

| $1M to $2M | 3.0x to 4.5x | 4.0x to 6.0x | 3.5x to 5.0x | 2.5x to 3.5x |

| $2M to $5M | 3.75x to 5.0x | 5.0x to 7.0x | 4.0x to 6.0x | 3.0x to 4.0x |

| $5M+ | 4.0x to 6.0x | 7.0x to 10.0x+ (platform tier) | 5.0x to 7.0x | 3.5x to 4.5x |

| $25M+ revenue scaled platform | 2.5x to 3.5x revenue multiple | 7.0x to 10.0x EBITDA | 0.87x to 1.5x revenue | 0.75x to 1.25x revenue |

Within each band, the precise multiple a buyer pays depends on six factors: practice area mix, owner-relationship concentration, recurring revenue share, financial reporting quality, marketing channel diversification (PI), and attorney bench depth. The cross-source mid-band figures are estimates within the published source ranges. Transactional and corporate boutiques typically trade at 0.5x to 1.5x revenue (Law Practice Exchange 2025) or 0.87x to 1.21x revenue blended (Peak Business Valuation 2025); IP and patent prosecution boutiques can clear 1.0x to 1.5x revenue when paired with retained-counsel relationships at Fortune 500 clients.

Recent disclosed law firm transactions (2023 to 2026)

| Acquirer / Investor | Target | Date | Value | Implied multiple |

|---|---|---|---|---|

| Fortress Investment Group | Rafi Law Services (MSO of Rafi Law Group) | April 2026 | $125M for minority stake; ~$450M MSO valuation | Not broken out; estimated high single digits to low double digits implied |

| Uplift Investors | Orion Legal MSO with Dudley DeBosier | January 22, 2026 | Not disclosed | Not disclosed; fund targets $10M to $40M EBITDA platforms |

| McDermott Will & Schulte (internal combination) | (merger of McDermott Will & Emery and Schulte Roth & Zabel) | Mid-2025 | Combined ~$2.8B 2024 revenue | Not a valuation deal |

| Inflexion Private Equity | DWF Group plc (UK) | October 2023 | £342M / ~$420M USD | ~0.9x EV / Revenue at FY April 2025 revenue £466M |

| Allegro Funds | Slater + Gordon (Australia) | April 2023 | A$78M / ~$52M USD | Public market valuation |

| General Catalyst | Eudia (legal AI platform with Arizona ABS) | February 2025 | $105M Series A | Pre-revenue legal AI play; not a law firm valuation |

Sources: Bloomberg Law (multiple 2025 and 2026 articles); BusinessWire and Houlihan Lokey transaction page on Uplift Investors / Orion Legal / Dudley DeBosier (January 2026); AZ Big Media and Legal Futures (April 2026 Rafi Law Services); ABA Journal and Financial Times (McDermott November 2025 and February 2026); Inflexion press release (October 2023); Global Legal Post (DWF revenue, 2025); Lawyers Weekly and Business News Australia (Slater + Gordon, February 2023); Artificial Lawyer and Eudia press release (September 2025). One disclosure note: most smaller PE-backed MSO deals and lateral acquisitions do not publish deal values, so the transaction table is genuinely thinner than HVAC. Most of what trades sub-$50M in the law firm market is not reported in the press.

The 14 Value Levers That Move Your Multiple (Ranked by Impact)

These are the levers that move law firm multiples in the 24 to 36 months before a sale. Each one has a current state, a target state, and an estimated financial impact. The ordering is by dollar impact per unit of effort, based on cross-source synthesis from Peak Business Valuation, The Law Practice Exchange, CSuite Financial Partners, LeanLaw, Arrowfish Consulting, Eton Venture Services, Holland & Knight, and ABA Model Rule commentary.

Lever 1: Build a transferable book by removing owner concentration

Current: Owner or managing partner owns 50%+ of client relationships and originates 60%+ of new matters. Target: No single attorney owns more than 30% of revenue. Documented intake process, centralized client relationships, partner team with portable books, junior attorneys with their own books. Impact: This is the single biggest valuation lever in law firm M&A. Buyers cite founder-dependence as the most common reason to discount Dallas boutique multiples from a 3x peak in 2022 down to 1.5x to 3x in 2025 (The Law Practice Exchange Dallas boutique data, 2025). On a $2M EBITDA firm, moving from a 3x multiple to a 5x multiple is the difference between $6M and $10M of sale price (CSuite Financial Partners, 2025). How: 24 months pre-sale, start migrating client relationships from the owner to associates and partners. Build internal handoff documents. Run quarterly client business reviews led by associates with the owner in supporting role. Track “originator” vs. “responsible” partner separately and shift the responsible partner away from the owner.

Lever 2: Move from cash to GAAP accrual accounting with monthly close

Current: Cash-basis books, annual tax return, no monthly close. Owner can describe profitability but cannot produce monthly P&L by practice area. Target: GAAP accrual books, monthly close in 15 days, P&L by practice area, CFO or fractional CFO function. Two to three quarters of clean accrual history before going to market. Impact: CSuite Financial Partners cites a specific example: a $2M EBITDA firm with cash-basis books trades at 3x ($6M); the same firm with GAAP accrual, monthly close, and CFO function trades at 5x ($10M). That is $4M of sale price on bookkeeping (CSuite Financial Partners, 2025). LeanLaw notes clean financials add 1.0x to 2.0x to a typical multiple (LeanLaw 2025). How: Engage a CPA firm that specializes in law firms 24 months pre-sale. Convert to accrual. Set up Clio Accounting, QuickBooks Online plus a law-firm accountant overlay, or Aderant or Elite 3E with proper revenue recognition rules. Build monthly close discipline.

Lever 3: Diversify marketing channels (PI specific)

Current: Single marketing channel above 35% of signed cases (often a TV ad campaign, a single medical-provider referral network, or a single paid-search account). Target: No channel above 35%. Mix of paid search, LSA, SEO, direct mail, TV and radio, referral, prior-client, and case management software intake automation. Impact: Channel concentration above 35% is one of six measurable factors that buyers use to set the multiple within the 3x to 10x band (CSuite Financial Partners, 2025). Estimate: moving from single-channel dominance to true diversification lifts the multiple by 1.0x to 2.0x for a $1M to $5M EBITDA PI firm, worth $1M to $10M of sale price. How: Year 1, build owned-channel SEO and review base. Year 2, add LSA and paid search at under $2,500 cost per signed case. Year 3, maintain channel mix discipline with quarterly channel-attribution reviews. Use Filevine, Litify, or CASEpeer for channel-attribution reporting.

Lever 4: Convert hourly to fixed-fee, retainer, or subscription where defensible

Current: 100% hourly billing. No recurring monthly engagement. Target: 20% to 40% of revenue from monthly retainer, fixed-fee bundle, or subscription engagement. Immigration shops can run payroll-based green-card volume contracts; ERISA shops can run monthly plan-administration retainers; family practices can offer flat-fee divorce packages; transactional practices can offer general counsel light at $5K to $15K per month. Impact: Recurring revenue is the law-firm equivalent of the HVAC maintenance plan. Estimate: 25%+ recurring revenue lifts the multiple by 0.5x to 1.5x EBITDA (cross-source synthesis from LeanLaw 2025, Peak Business Valuation 2025, and Arrowfish Consulting 2025). How: Start with two retainer tiers for existing clients. Document scope by tier. Auto-renew with stored payment. Train associates on retainer scope management. Build a retainer-book KPI dashboard inside Clio or Aderant.

Lever 5: Put a managing attorney or COO in the chair before exit

Current: Owner does 80%+ of management decisions, signs every check, attends every major client meeting, runs intake personally. Target: Managing attorney or non-attorney COO in place 12 to 24 months before exit. Owner doing under 30 hours per week of operational work. Owner unplugged for 2 to 4 weeks as a stress test. Impact: Same direction as Lever 1 but distinct: this is operational dependence, not relationship dependence. Estimate: removing owner operational dependence moves a $1M to $3M EBITDA firm from the 3x to 4x band into the 4x to 5x band, worth $1M to $4M of price. How: 18 to 24 months pre-sale, hire or promote a managing attorney with operational authority. Document SOPs for intake, conflict-check, engagement letter preparation, matter close, fee escalation, partner reviews. Stress-test with a two-week owner vacation.

Lever 6: Practice management software adoption with clean data

Current: Spreadsheets, paper files, no centralized matter tracking, anecdotal billable utilization. Target: Clio for general practice and mid-size; Filevine, Litify, CASEpeer, or Smokeball for PI; Aderant or Elite 3E for $10M+ revenue firms; NetDocuments or iManage for document management. Monthly KPI dashboard. Impact: Estimate +0.25x to 1.0x multiple uplift, driven mostly by the speed and credibility of data-room responses during diligence. Clio dominates mid-size general practice with roughly 18% market share and 250+ integrations; the top five providers hold 42% of the global market (Business Research Insights 2025; My Legal Academy “Case Management Software Comparison 2026”). How: Budget $25K to $150K implementation cost plus per-attorney license. Force adoption through billing requirement (no time gets into payroll unless entered in the system). Run quarterly data-quality audits.

Lever 7: Tighten attorney non-compete and non-solicit posture within Rule 5.6 limits

Current: Partnership agreement has unenforceable attorney non-compete provisions, no non-solicit on clients or staff, no documented covenant practices. Target: Compliant non-solicit covenants (generally permissible under Rule 5.6 if they do not effectively restrict practice), Rule 1.17 sale-of-practice consent framework prepared in advance, retention bonus structure for key attorneys triggered by closing. Impact: Reduces the buyer’s perceived risk of attorney walk-off after close. Estimate: directly translates to +0.5x to 1.5x on multiple at the close (ABA Model Rule 5.6; Washington State Bar News RPC 5.6(a) March 2023; North Carolina State Bar Rule 5.6 commentary; Seyfarth Shaw trade-secret analyses). How: Bring outside ethics counsel into the partnership agreement amendment 18 to 24 months pre-sale. Build a retention bonus pool sized at 5% to 10% of deal value, paid 12 to 36 months post-close to key attorneys.

Lever 8: EBITDA add-back hygiene with attorney compensation normalization

Current: Owner mixes personal expenses through the firm with no documentation; partners take guaranteed payments that include market salary plus profits with no separation; related-party rent or vendor contracts at above-FMV. Target: Every potential add-back documented with the underlying invoice or payroll record; owner and partner compensation normalized to market-rate managing partner salary ($500K to $1M per CSuite 2025); related-party rent restruck to FMV with appraisal on file. Impact: Every defensible dollar of adjusted EBITDA gets multiplied at exit. On a 5x multiple, $200K of clean add-backs (owner over-comp, owner family payroll, owner vehicle, one-time legal) adds $1M of sale price (Morgan & Westfield QoE guide 2025; CSuite Financial Partners 2025; Auxo Capital Advisors QoE buyer flag guide). How: Adopt a monthly add-back log starting today. Document the business purpose of every charge. Get a FMV rent appraisal if the partner owns the real estate and the firm rents it. Establish a documented partner-comp policy that separates market salary from profit allocation.

Lever 9: Working capital normalization with WIP and AR discipline

Current: WIP and AR accumulate, write-offs are sporadic, cash conversion cycle is 9 to 12+ months for PI, 90+ days for transactional or hourly. Target: TTM-average working capital stable and predictable; WIP aged under 60 days; AR aged under 90 days; case-cost advances tracked separately from operating receivables; deferred fee income on contingent matters disclosed as a near-term receivable schedule. Impact: The working capital peg is set off TTM average (typically the last 6 to 12 months per BDO and Morgan & Westfield NWC guides). A volatile working capital pattern lets the buyer set a higher peg, which subtracts from purchase price. Estimate: poor WC discipline can cost 2% to 5% of enterprise value at close. For PI specifically, the 9 to 12+ month cash conversion cycle requires explicit treatment in the SPA. How: Tighten AR collection cycle, set monthly WIP-to-bill targets, isolate case-cost advances on the GL, build a separate aging report for contingent-matter cost recovery.

Lever 10: Real estate decision (own or lease, and the sale-leaseback option)

Current: Partner-owned real estate held in the same entity as the law firm, or in an LLC at above-FMV rent. Target: Real estate in a separate LLC at FMV NNN lease to the operating firm, with a clear path for the buyer to either assume the lease or buy the real estate separately. Impact: Separating real estate often lifts the implied EBITDA multiple on the operating firm because the buyer is not forced to underwrite real estate exposure. A sale-leaseback can release up to 100% of property market value as cash, vs. 70% to 80% LTV via traditional financing (Plante Moran sale-leaseback primer; Northmarq sale-leaseback guide; W. P. Carey blog). Estimate impact: holding real estate separately at FMV typically adds 0.5x to 1.0x to the operating firm multiple. How: Get a FMV market rent study now. Restruck rent to FMV. Decide before going to market whether the real estate is part of the deal or held back.

Lever 11: State expansion and multi-state licensing

Current: Single-state license. Single-state attorney bench. Target: Bar admissions in 4+ states across attorney bench, especially in high-PE-interest states (Arizona, Florida, Texas, California, Pennsylvania, North Carolina, Georgia, Tennessee). Impact: Multi-state coverage gives the buyer immediate growth optionality without lateral hires. Estimate: +0.5x to 1.5x multiple for buyers with platform expansion mandate. Sun Belt and growth-state coverage attracts the strongest PE buyer demand. How: 24 months pre-sale, sponsor select attorneys to sit for additional state bars (UBE score transferability covers approximately 40 jurisdictions). Document pro hac vice patterns to identify which states would best add to the bench.

Lever 12: Case-cost finance and medical-lien relationships (PI specific)

Current: Owner-financed case costs and medical liens on a haphazard basis; no documented finance relationships. Target: Documented relationships with Esquire Bank (case-cost financing), Burford Capital (litigation finance for large cases), and medical-lien finance providers; clear policy on which cases get external finance vs. firm-financed. Impact: Reduces working capital intensity, improves cash conversion cycle, and gives the buyer a runway to scale case volume post-close without committing additional capital. Estimate: +0.25x to 0.75x multiple in PI for firms with mature finance relationships. How: Establish Esquire Bank or comparable depository relationship 12+ months pre-sale; document case-cost finance policy; map case-stage to finance-source decision matrix.

Lever 13: Document automation and AI adoption (transactional, immigration, M&A diligence)

Current: Lawyers draft from scratch; no template library; no AI-assisted review. Target: Document automation through Lexion, Ironclad, NetDocuments, or HotDocs; AI-assisted contract review and due diligence (EvenUp for PI demand packages, Eudia-style AI for M&A diligence, Harvey AI for general drafting). Impact: Direct EBITDA growth through fewer attorney hours per matter, plus a defensible tech-forward story in the CIM. J&Y Law in Los Angeles reported saving 320 attorney hours per week through EvenUp AI adoption (BusinessWire, April 2026). Estimate: 5% to 15% EBITDA lift from mature AI adoption in 24 months. How: 18 months pre-sale, identify the highest-volume document types in the firm and pilot one document automation tool against them. Measure attorney hours saved.

Lever 14: Pre-sell QoE

Current: Buyer’s accountant runs the only QoE, after LOI, in the buyer’s favor. Target: Sell-side QoE in hand before the CIM goes out; adjusted EBITDA documented, defensible, and tied to invoices. Impact: Cost $30K to $50K typical for a PI firm, $50K to $75K for multi-practice or multi-state firms. Can lift price by $1M+ per turn of multiple gained on a $2M to $5M EBITDA firm. How: See the QoE section below.

Want to grow your firm to maximize value before exiting?

We connect law firm partner-owners with legal-services operations experts in our partner network who run 12 to 24 month pre-sale optimization engagements. The engagement pays for itself in incremental sale price.

What PE Asks Before They Send an LOI (The Pre-LOI Diligence Stack)

Before a PE firm or MSO investor commits to a letter of intent, they ask for a focused diligence package. The list below is the real ask from a 2026 PE-MSO investor targeting a plaintiff PI firm in CT Acquisitions’ pipeline. The “why” and “how to prepare” expand each item to what is typical across the industry.

1. Income statements: trailing 24 to 36 months plus LTM

Why PE asks: They build LTM adjusted EBITDA from these. For PI firms the LTM number depends heavily on which fiscal months captured large settlements; PE wants to see that the underlying engine, not a single jury verdict, drives the trend. For transactional and IP firms, PE wants to separate one-time M&A spikes from base retainer revenue.

How to prepare: Accrual-basis P&L by month. Practice-area P&L (PI vs. workers comp vs. premises vs. med-mal, or transactional vs. litigation vs. regulatory). Reconcile to tax returns. For PI firms, isolate fee-only revenue from cost-recovery line items.

2. Balance sheet at latest month with WIP and AR aging

Why PE asks: Two purposes. First, sizing the working capital peg they will set in the SPA. Second, identifying net debt and debt-like items (the largest one for law firms: case-cost advances on contingent matters, which sit on the balance sheet as receivable from the case but are debt-like for valuation). Unbilled WIP and accounts receivable aging beyond 90 days are also scrutinized.

How to prepare: Tie balance sheet to trial balance. Isolate case-cost advances separately from operating receivables. Age AR by client matter. Disclose the firm’s realization rate (collected fees divided by billed fees) and net realization rate (collected fees divided by standard billing rates).

3. Adjusted EBITDA bridge with addback documentation

Why PE asks: Law firms have especially heavy adjustments because partner compensation gets restated to market-rate associate or managing partner salary. CSuite notes the founder typically draws $500K to $1M post-transaction as managing partner, with the residual above that adding back to EBITDA (CSuite Financial Partners, 2025).

How to prepare: Bridge from book EBITDA to adjusted EBITDA, line by line. Common law-firm adjustments: owner compensation above market, owner family payroll, owner vehicle and personal travel, owner health insurance and country-club, one-time large settlements (PI), one-time litigation costs the firm bore for its own defense, software conversion one-time costs, related-party rent at above-FMV. References: Morgan & Westfield QoE; Auxo Capital Advisors QoE buyer flag guide.

4. Anonymized attorney and staff roster (titles, bar admissions, books)

Why PE asks: Two risks. First, attorney portability under ABA Model Rule 5.6 (attorney non-competes restricting the practice of law are unenforceable in 47 of 50 states; only narrow exceptions tied to a Rule 1.17 sale of practice or a retirement plan are enforceable). Second, key-rainmaker risk: if 60% of the book comes from one partner, that partner walking is a near-total deal kill.

How to prepare: Roster columns include role, bar admissions by state with admission dates, hire date, employment vs. of-counsel vs. contract, comp structure (salary, bonus formula, eat-what-you-kill split, origination credit), and any active non-compete or non-solicit clause with enforceability commentary. Disclose the book of business held by each partner. Calculate and disclose attorney 24-month retention rate and the percent of revenue held by the top three attorneys.

5. Matter or case inventory and revenue mix by practice area

Why PE asks: For PI firms this is the single most diagnostic exhibit. They want case count by stage (pre-litigation, in litigation, in trial, on appeal, settling, closed), expected fee per case, weighted-probability fee, average time to settlement, and average case life. For non-PI firms, they want matter count by client, average matter fee, retention rate of repeat clients, billable hours by attorney, billable utilization, and realization.

How to prepare: Pull straight out of Clio, Filevine, Litify, Smokeball, MyCase, PracticePanther, Aderant, or Elite 3E. For PI: case stage waterfall report, settlement-time distribution chart, average policy limit by case type, marketing channel attribution per signed case. For transactional or IP or immigration: matter count by client, matter mix by practice area, hours and fees by attorney, billable utilization (target 1,650 to 1,800 hours annually per associate, 1,400 to 1,600 per partner per industry benchmarks).

6. Client or referral-source concentration (top 10)

Why PE asks: Concentration is even more sensitive for law firms than HVAC because the client relationship sits with an individual lawyer, not the firm name. If a top client books $400K of fees per year and the relationship sits with a single partner who walks, the firm loses that revenue overnight. For PI firms, “concentration” is usually replaced by “referral-source concentration” (top medical providers, marketing agencies, prior clients) because cases come and go but the referral spigot is the steady-state asset.

How to prepare: Top 10 clients by 24-month revenue contribution. Top 10 referral sources for PI. Specifically: who owns the relationship (partner X, partner Y, the firm brand). Note any documented retainer or referral agreement.

7. Recurring revenue snapshot (retainer clients, subscription engagements, fixed-fee programs)

Why PE asks: Recurring monthly retainer or subscription revenue is the law-firm equivalent of the HVAC maintenance plan. Higher recurring share lifts the multiple. Estimate: a transactional firm with 30%+ revenue from monthly retainers can move from the 3x to 4x EBITDA band into the 4x to 5x band on the recurring quality alone (cross-source synthesis).

How to prepare: Monthly retainer count, average monthly retainer revenue, retainer client churn rate, plan-mix breakdown if multiple tiers exist (e.g., “general counsel light” vs. “general counsel premium”), 12-month and 24-month renewal rate.

8. Marketing spend, channel mix, cost per signed case (PI)

Why PE asks: Marketing is the single biggest controllable expense line for PI firms and the single biggest risk lever. PE wants channel-by-channel CAC, conversion rate by source, and the relationship to settled fee. Industry benchmarks: PI cost per signed case typically $2,500 to $3,500 for auto accident, $5,000 to $8,000 for medical malpractice, $2,000 to $3,000 for premises liability (Practice Proof 2025; OnTheMap 2025; Savvy Law Firm Marketing 2025).

How to prepare: Channel mix table (paid search, LSA, SEO, direct mail, TV, radio, referral, prior client) by spend and signed cases. Cost per signed case by channel. CPC ranges $70 to $250 in PI (Practice Proof 2025). Sign rate from initial contact: industry benchmark 65% to 75% on sent retainer agreements (LawFirm-CMO 2025).

9. IOLTA trust account compliance certification and audit history

Why PE asks: IOLTA mismanagement is a near-instant deal-kill. State bars conduct random and for-cause trust account audits and any open finding or pending disciplinary action against the firm or any partner from a trust account discrepancy will surface in confirmatory DD (ABA, “A Guide to Ensuring IOLTA Account Compliance”, 2024; California State Bar Client Trust Account Protection Program; Federal Bar Association IOLTA compliance guide).

How to prepare: Three-year reconciliation history. Annual compliance certifications filed with the state bar. Any open inquiries documented and resolved before going to market.

10. State bar disciplinary records, malpractice claims history, conflict-check process

Why PE asks: Open or recent malpractice claims, state bar discipline, and reportable settlements all change the risk profile and the E&O insurance pricing post-close. Approximately 4% of US private-practice lawyers face a malpractice allegation in any given year (ABA via Sakkas Cahn & Weiss reference 2025); defense costs on a claim with merit can exceed $25,000 and claims can take 6 to 24 months to resolve. Conflicts-of-interest portfolio mismatch is the second-most-cited deal architecture problem in law firm M&A.

How to prepare: Full disclosure of last 7 years of E&O claims, disciplinary inquiries, and bar complaints. E&O policy declarations page with extended reporting period (tail) terms. Written conflict-check policy. Last 3 years of conflict logs. Acknowledgement of any active matters where conflict was waived in writing by clients.

11. Partnership agreement, capital accounts, deferred income, referral splits

Why PE asks: Partnership agreement governs capital account treatment, profit allocation, withdrawal rights, and assignability. For PI firms with substantial contingent-fee receivables (cases signed but not yet settled), the agreement controls how that future stream gets divided in a partial-partner exit. PE will not assume the firm without amendments that allow the new structure (whether ABS, MSO, or strategic absorption).

How to prepare: Counsel-reviewed partnership agreement with amendments documented. Capital account schedule by partner. Schedule of contingent-fee receivables and how each is split. Schedule of referral fee agreements with other firms.

Confirmatory Diligence (After You Sign the LOI)

Once an LOI is signed and exclusivity starts (typically 45 to 90 days for a law firm deal, although Rule 1.17 client-notice windows can push the closing timeline 3 months longer than HVAC or dental), the buyer runs the following parallel workstreams. This is the depth of inspection your firm will undergo. If anything was hiding, it surfaces here.

- Quality of Earnings (QoE). Outside accounting firm runs revenue cut-off testing focused on contingent-fee recognition (PI), retainer cycle billing, and matter-write-off patterns. Working capital trend analysis. Expense normalization with focus on partner compensation. Cost: $30K to $50K for sell-side QoE on a PI firm at typical size, up to $75K for multi-entity or multi-state practices (CSuite Financial Partners, 2025; Eton Venture Services, 2025).

- Client and matter concentration analysis. Calls with top accounts (subject to Rule 1.17 client-consent constraints), engagement letter review for change-of-control and assignment clauses.

- Tech stack and IT systems audit. Clio, Filevine, Litify, Smokeball, Aderant, Elite 3E, NetDocuments. Data quality, license counts, integration capability with the buyer’s platform.

- Legal and regulatory. State bar entity good standing in every state; license verification for every attorney with disciplinary record check; malpractice claims history with E&O insurance limits and tail coverage availability; trust account audit and IOLTA compliance documentation; conflict-check policy and recent conflict logs; partnership agreement and capital account schedule; Rule 1.17 client-notice planning (the law-firm-specific item with no equivalent in HVAC).

- HR and payroll. Attorney W-2 vs. 1099 vs. partnership-distribution classification audit, paralegal and staff classification, I-9 compliance, wage-and-hour exposure on non-exempt support staff.

- Tax. Federal income, payroll, and any state-level legal services taxes (most states do not tax legal services, but a handful tax them in certain situations).

- Real estate. Office lease assignment clauses; multi-state office locations and lease renewal calendar.

Why You Should Pay for Your Own Quality of Earnings Before Going to Market

A sell-side QoE is the firm’s own outside accountant’s QoE, paid for by the firm, before going to market. It does three things: pre-empts the buyer’s QoE by getting to the adjusted EBITDA number first with documentation; surfaces issues you can fix before the buyer sees them (revenue cut-off on contingent fees, working capital normalization, addback support); tightens the EBITDA number you take to market, which directly drives the headline price. Law-firm-specific add-back items (partner compensation normalization, contingent-fee receivables, case-cost advances, related-party rent) require defensible documentation that takes months to assemble.

Cost

- $30K to $50K typical for sell-side QoE on a PI firm at $1M to $5M EBITDA (CSuite Financial Partners, “Quality of Earnings for Law Firms: The What and Why”, 2025).

- $50K to $75K for multi-practice or multi-state law firms with more complex revenue recognition (estimate based on Eton Venture Services 2025 baseline plus law-firm complexity premium).

- Up to $150K for firms with multiple entities, multi-state operations, contingent-fee portfolios with thousands of cases, or messy books (estimate based on Eton 2025 upper-bound).

ROI

Worked example: $2M EBITDA PI firm. Moving the multiple from 3x to 5x via clean financials and documented add-backs equals $4M of additional sale price (CSuite Financial Partners, 2025). A $40K QoE investment that supports that 2x lift is a 100x return. Industry-cited mirror example: a PI firm with cash-basis books and an April tax return trades at 3x; the same firm with GAAP-compliant accrual accounting, monthly closes, and CFO function trades at 5x.

Deal-Killers That Re-Trade Law Firm Transactions (Avoid These)

These are the recurring kill-shots cited across law firm M&A advisory content and confirmatory diligence checklists. Most are fixable in 12 to 24 months. None are fixable in 30 days. Several are unique to law firms and have no analog in any other vertical.

1. ABA Model Rule 5.4 and the corporate practice of law doctrine

The most common deal-architecture failure: the buyer wants direct equity in the law firm, but the operating state prohibits non-lawyer ownership. Only Arizona, Utah, Washington DC, and Puerto Rico allow direct non-lawyer ownership. In every other state, the deal has to be restructured into an MSO sitting beside the lawyer-owned PLLC, often validated by reference to Texas Ethics Opinion 706 (February 2025). Failure to architect this up front can add 3 to 6 months and 7-figure legal cost mid-deal (DLA Piper, “MSOs vs. ABS: Two Models for Investment in Law Firms”, January 2026; Sidley Austin, November 2025; Holland & Knight, August 2025).

2. Attorney non-competes unenforceable under ABA Model Rule 5.6

ABA Model Rule 5.6 makes most attorney non-competes restricting the practice of law unenforceable in 47 of 50 states. Only narrow exceptions: restrictions tied to a Rule 1.17 sale of practice, or retirement-benefit-conditional restrictions. If the firm relies on non-competes to retain key partners post-close, the buyer treats those attorneys as flight risk and prices it in (Washington State Bar News, March 2023; Seyfarth Shaw analyses; North Carolina State Bar commentary).

3. Rule 1.17 client-consent friction

Under Model Rule 1.17, adopted in most states, client files cannot transfer in a sale of practice without written notice to each client with a 90-day window for objection. Clients have the right to retain other counsel. This is a law-firm-specific deal-kill that has no analog in HVAC or dental. Buyers price in expected client attrition; estimate: 5% to 15% of clients exercise the right to switch (estimate based on ABA Model Rule 1.17 commentary and state-bar guidance; varies by state, by practice area, and by client transferability).

4. IOLTA trust account compliance gaps

Random or for-cause state bar audits surface in confirmatory DD. California’s Client Trust Account Protection Program (CTAPP) requires annual registration, self-assessment, and certification. Settlement examples include public state bar discipline actions with named attorneys facing suspension over commingling or shortages. Source: California State Bar CTAPP; ABA IOLTA compliance guide 2024; LawPay 2025; Accounting Atelier 2026.

5. Malpractice claims history and pending E&O claims

Open or recent claims push E&O insurance pricing up materially and may trigger an indemnity holdback. Approximately 4% of US private-practice lawyers face a malpractice allegation annually; defense costs exceed $25K per merited claim and resolution takes 6 to 24 months. Jaffe Raitt Heuer & Weiss was hit with a $5M malpractice verdict in a transactional matter where the firm allegedly failed to advise on a $3.26M underfunded pension liability (trade press 2025). Source: ABA Lawyers’ Professional Liability resources; Sakkas Cahn & Weiss 2025; ALPS Insurance; Embroker.

6. State bar disciplinary records on key partners

Any active disciplinary inquiry or recent public discipline on a key partner is a near-instant deal-kill or a material price discount. Discoverable through the state bar’s public discipline database; the buyer will run a full check during DD.

7. Conflicts-of-interest portfolio mismatch

A combined firm’s matter portfolio cannot conflict with the buyer’s portfolio. ABA Model Rule 1.7 governs concurrent conflicts; Rule 1.9 governs former-client conflicts. Buyer DD includes a side-by-side matter list reconciliation; major conflict findings can require dropping clients or restructuring engagements, both of which destroy value.

8. Partnership agreement assignability and capital account complexity

Partnership agreements that prohibit assignment, or have complex capital-account schemes (subordinated capital, retained earnings owned by senior partners), can require amendments before close. Senior partners may resist amendments that move value to the firm-level transaction.

9. Contingent fee income recognition and case-cost advance treatment (PI specific)

The QoE will test how the firm recognizes revenue on contingent matters. Some firms aggressively recognize fees at settlement signature; the QoE may push that recognition to actual cash collection. Case-cost advances (cash the firm has paid to fund discovery, expert witnesses, medical-record retrieval) may be reclassified from operating asset to debt-like, reducing the EV after the working capital peg (Morgan & Westfield QoE guide 2025).

10. Marketing channel concentration above 35% (PI specific)

Channel concentration above 35% triggers buyer pushback and price discount of 1.0x to 2.0x EBITDA (CSuite Financial Partners, 2025). Common patterns: 60% of cases coming from a single TV ad campaign; 50% from a single medical provider referral network; 70% from a single paid-search agency.

11. Unfunded partner pension or deferred compensation obligation

23% of partners at Am Law 200 firms responded in a Major Lindsey & Africa survey that their firm has a pension plan that is not funded (MLA Global Law Firm Succession Planning analysis, 2024 to 2025). For a sub-Am-Law firm in M&A, an unfunded deferred-comp liability to retiring partners becomes a debt-like item that reduces purchase price dollar for dollar.

12. Real estate at above-FMV related-party rent

Most law firms have at least one partner who owns the office building through a related LLC and charges above-market rent. The QoE strips this back to FMV and the buyer prices the deal off the FMV rent, often costing the seller a six-figure value adjustment.

13. Owner-rainmaker concentration above 50%

If 50%+ of revenue comes from clients originated by a single partner who is also the seller, the buyer treats the entire firm as a flight risk. Typical resolution: a multi-year earn-out tied to client retention and a separate retention payment to the owner, which delays cash to the seller and shifts risk to them.

14. Multi-state regulatory exposure on cross-discipline services

For firms that offer estate planning, financial planning, or tax consulting alongside legal services, the cross-border MSO and ABS rules complicate the deal. California’s AB 931 explicitly forbids attorneys from sharing fees with out-of-state ABS firms (DLA Piper, January 2026). Multi-state firms need to map the regulatory matrix before going to market.

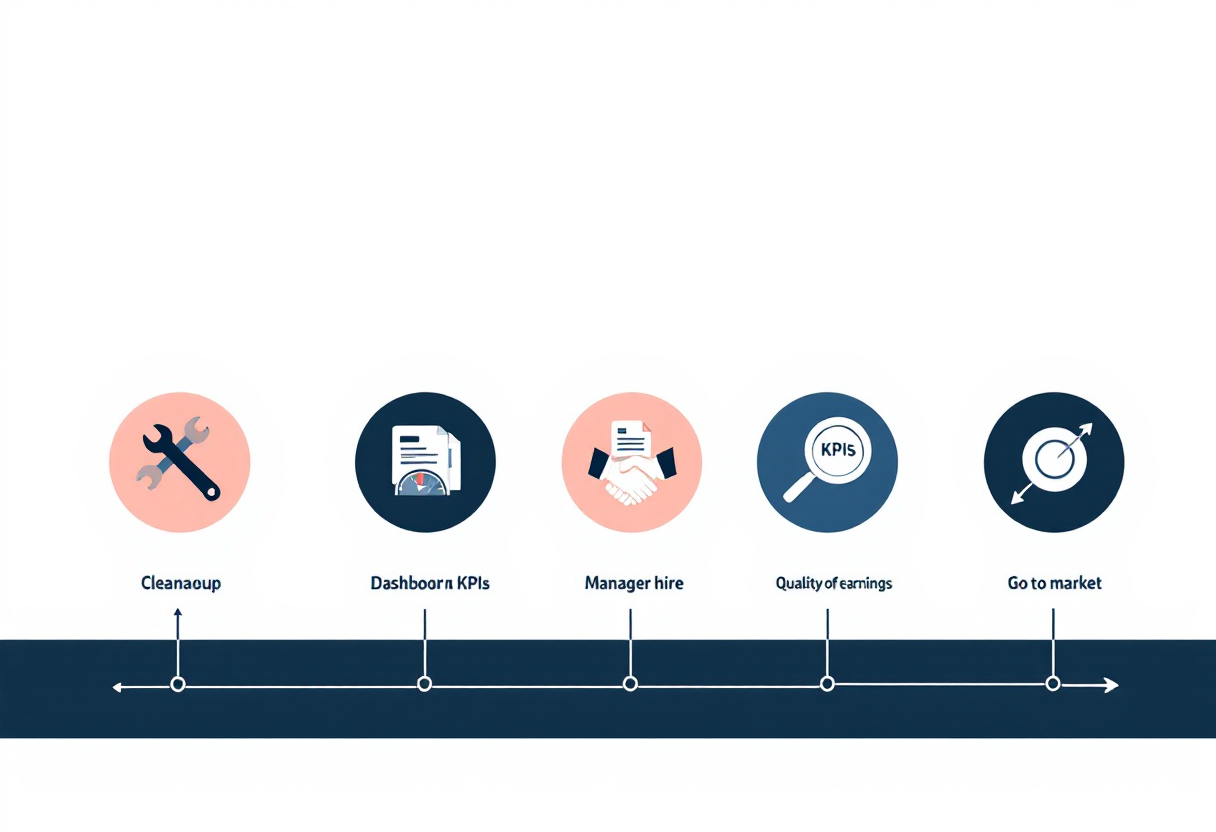

The 36-Month Exit Prep Timeline

T-36 months: Cleanup phase

- Switch to GAAP accrual basis if still on cash basis; engage a law-firm-specialist CPA

- Begin migration to a practice management platform appropriate to size (Clio for general; Filevine, Litify, or CASEpeer for PI; Aderant or Elite 3E for $10M+ revenue)

- Start tagging every potential EBITDA add-back as it happens; build the add-back log

- Run a partnership agreement review with outside ethics counsel; identify assignability, capital account, and non-solicit issues

- Begin client relationship handoff from owner to associates and partners on a documented schedule

- Audit IOLTA trust account history for the last 3 years; resolve any open inquiries with the state bar

- Get a FMV rent appraisal if the firm rents from a related-party LLC

- Review malpractice and E&O insurance coverage and tail terms

- Build state-by-state attorney bar admission grid; identify gaps relative to PE buyer geography

- Decide whether the eventual deal is most likely Arizona ABS, MSO + PLLC, or strategic merger; align early structuring with ethics counsel

T-24 months: Financial discipline and KPI infrastructure

- Managing attorney or COO onboarded with operational authority

- Monthly close in 15 days, P&L by practice area every month

- KPI dashboard built. For PI: case inventory by stage, marketing channel attribution, cost per signed case, sign rate, average settlement cycle, average policy limit, settlement realization rate. For non-PI: billable utilization, realization rate, matter-to-revenue ratio by attorney, retainer renewal rate

- Launch retainer, subscription, or fixed-fee programs if no recurring revenue exists

- Marketing diversification kick-off; target no channel above 35% by month T-12

- Document SOPs for every operational role (intake, conflict-check, engagement letter, matter open, billing, matter close)

- Pricing review: standard hourly rates raised 5% to 8%; alternative fee structures piloted

- Begin client diversification work if any top client is above 15% of revenue

- Build the add-back bridge as a living document

T-12 months: QoE-ready close discipline, eliminate owner dependence

- Owner steps out of daily management; managing attorney runs the firm

- Owner takes a 2 to 4 week unplugged vacation as the stress test

- Run the sell-side QoE (budget $30K to $75K)

- Tighten balance sheet: clean AR, write off dormant WIP, isolate case-cost advances and contingent receivables

- Final partnership agreement amendments completed

- Final compliance scrub (IOLTA, state bar, malpractice, E&O, conflict logs)

- Lock in 12 months of clean accrual-basis P&L by practice area for the CIM

- Buyer list research: name 25+ active buyers from the platform list plus relevant strategic acquirers in the firm’s specialty

T-6 months: Pre-marketing prep

- Engage an M&A advisor or law-firm-specialist sell-side advisor (Fairfax Associates, Altman Weil, Olmstead & Associates, The Law Practice Exchange, Auxo Capital Advisors, CSuite Financial Partners, Houlihan Lokey for $100M+ deals, Stifel for mid-market, M&A boutiques specializing in legal services). Typical fee structure: monthly retainer $25K to $75K credited against success fee of 4% to 8% of enterprise value (estimate based on standard mid-market M&A fee schedules)

- CIM drafted from the QoE and operating model; CIM must address practice area mix, attorney bench by state, top 10 clients or referral sources, retention metrics, IOLTA compliance certification, malpractice history, partnership structure, and proposed deal structure (ABS, MSO, or strategic absorption)

- Teaser drafted (anonymized 1-pager)

- Buyer list finalized

- Virtual data room populated with everything from the pre-LOI and confirmatory sections above

- Management presentation deck built and rehearsed

- Begin Rule 1.17 client-notice planning with ethics counsel; identify which clients are likely to consent to transfer and which are flight risks

T-3 months: Go to market

- Teaser distributed; NDAs collected; CIMs distributed

- IOIs collected 2 to 3 weeks after CIM goes out

- Narrow to 4 to 6 finalists for management meetings

- Management meetings; LOIs solicited

- Select LOI; sign with exclusivity (typically 45 to 90 days)

- Enter confirmatory diligence; close

- After signing the Definitive Purchase Agreement, send Rule 1.17 client notices with 90-day objection window (in jurisdictions that require it)

End-to-end from engagement to close: 9 to 14 months in a well-run process. The Rule 1.17 client-notice window can push the closing timeline 3 months longer than HVAC or dental equivalents (Auxo Capital Advisors sell-side process guide 2025; Wall Street Prep sell-side primer; The Law Practice Exchange sale process guides; ABA Model Rule 1.17).

Frequently Asked Questions

How long should I plan for before selling my law firm to a private equity buyer or strategic acquirer?

Owners who get top-quartile pricing start preparing 24 to 36 months before going to market. The minimum useful prep window is 12 months, because most of the high-leverage levers (lifting the owner-relationship share below 30%, installing a managing attorney, converting a transactional book to retainer revenue, running a sell-side QoE) need 12+ months of clean trailing-twelve-months data to be credible to a buyer. Partner-owners who try to sell in under 6 months typically leave 20% to 40% of enterprise value on the table.

What is a realistic EBITDA multiple for a $2M EBITDA personal injury or transactional law firm in 2026?

For a $2M EBITDA plaintiff personal injury firm in 2026, the EBITDA multiple range is 5.0x to 7.0x in the standard band, and can stretch to 7.0x to 10.0x+ at the platform tier with diversified marketing channels, mature case-cost finance relationships, and 35%+ multi-state attorney coverage (CSuite Financial Partners, 2025; Abogados Now, 2025). For a $2M EBITDA transactional or business law firm, the range is 3.75x to 5.0x EBITDA, or roughly 0.87x to 1.5x revenue depending on retainer mix and client retention. IP and patent prosecution boutiques can clear 1.0x to 1.5x revenue when paired with retained-counsel relationships at Fortune 500 clients. Insurance defense and family law anchor in the 3.0x to 4.0x EBITDA range at this size (Peak Business Valuation, 2025; The Law Practice Exchange, 2025).

Can private equity actually own my law firm in my state, or do I have to use an MSO?

Direct PE ownership of a US law firm is only legal in four jurisdictions as of May 2026: Arizona (which eliminated Rule 5.4 effective January 1, 2021 and has approved 136 Alternative Business Structures), Utah (regulatory sandbox launched August 2020, with 11 authorized entities as of April 30, 2025), Washington DC (limited non-lawyer ownership since 1991), and Puerto Rico (49% non-lawyer ownership since 2025). In all 46 other US jurisdictions, ABA Model Rule 5.4 prohibits non-lawyer ownership and fee-sharing. The standard workaround is the MSO (Managed Services Organization) structure: an investor-owned company sits next to the lawyer-owned PLLC and provides back-office services to the firm under a long-term services agreement. Texas Ethics Opinion 706 (February 2025) confirmed the MSO model is permissible when structured correctly. The MSO route is the dominant pathway for PE capital into US law firms in 2026 (DLA Piper, January 2026; Holland & Knight, August 2025; Sidley Austin, November 2025).

What percentage of recurring revenue do PE or strategic buyers want to see in a transactional or business law practice?

20% to 40% of revenue from monthly retainer, fixed-fee bundle, or subscription engagement is the band that meaningfully lifts the multiple. Estimate: 25%+ recurring revenue lifts the multiple by 0.5x to 1.5x EBITDA on a transactional book (cross-source synthesis from LeanLaw 2025, Peak Business Valuation 2025, and Arrowfish Consulting 2025). Recurring-revenue mechanisms by practice area: general counsel light retainer at $5K to $15K per month (transactional); payroll-based green-card volume contracts (immigration); monthly plan-administration retainers (ERISA); flat-fee divorce packages (family); annual estate-planning subscription (trusts and estates). The buyer is looking for revenue that does not depend on a single matter and does not depend on the owner closing the next deal.

Will my attorneys stay after the sale? Are non-compete agreements enforceable in law firm M&A?

ABA Model Rule 5.6 makes most attorney non-competes restricting the practice of law unenforceable in 47 of 50 states. Only narrow exceptions: restrictions tied to a Rule 1.17 sale of practice, or retirement-benefit-conditional restrictions. This means a buyer cannot rely on a standard non-compete to keep your senior partners in their seats post-close. The mechanisms that actually work are retention bonuses (typically a pool sized at 5% to 10% of deal value, paid 12 to 36 months post-close to key attorneys), equity rollover into the buyer’s structure, and Rule-5.6-compliant non-solicit clauses on clients and staff. Plan the retention structure 18 to 24 months pre-sale with outside ethics counsel (ABA Model Rule 5.6; Washington State Bar News, March 2023).

How does Rule 1.17 affect my law firm sale and what is the client-consent process?

ABA Model Rule 1.17, adopted in most states, requires written notice to every affected client when a law practice is sold, with a 90-day window for the client to object or to retain other counsel. The notice must specify the proposed sale, the right to retain other counsel, and the client’s right to take possession of their file. Sellers cannot transfer files for clients who do not respond after the notice period only in jurisdictions where presumed consent is permitted; some states (and the California analogue under Rule 1.17) require affirmative client consent. Plan on 5% to 15% client attrition through this process (estimate based on ABA Rule 1.17 commentary and state-bar guidance; actual rate varies by state, practice area, and client transferability). Buyers price this attrition into the deal, and the timeline adds roughly 3 months to closing relative to non-law verticals. Begin Rule 1.17 client-notice planning with ethics counsel at month T-6 (Mass.gov Rules of Professional Conduct Rule 1.17; North Carolina State Bar Rule 1.17; DC Bar Rule 1.17; California State Bar Rule 1.17 Executive Summary).

What to Do Next

The law firm partner-owners who get the top-quartile multiple all do the same three things. They start preparing 24 to 36 months before they want to be out. They put a managing attorney or COO in place 12+ months pre-sale and migrate client relationships off the owner. And they invest in a sell-side QoE before any buyer sees a CIM.

Underneath those three moves sits the law-firm-specific work that other verticals do not need to do. Align the deal structure (Arizona ABS, MSO + PLLC, or strategic merger) with ethics counsel at month T-36, not month T-3. Resolve every open IOLTA inquiry and state bar disciplinary item before going to market. Map the Rule 1.17 client-notice plan ahead of time, with named flight-risk clients identified. Normalize partner compensation to a market-rate managing partner salary so the EBITDA bridge holds up under a QoE. None of this is fast work, and none of it can be done in the last 90 days.

If you are 12+ months from a potential exit and want a structured pre-sale optimization roadmap, CT Acquisitions has legal-services operations specialists in our partner network who run multi-quarter prep engagements. If you are 6 to 12 months out and ready to start the sell-side process, our M&A advisory team runs the buyer outreach. Buyers pay our fee, not you. Either way, the first 30 minutes are free.

Ready to talk?

Schedule a 30-minute exit-readiness call

Or read more: Sell Your Law Firm (active sale guide) | Buying a Law Firm (buyer’s playbook) | Private Equity in Law Firms 2026: MSO + ABS Structures

Ready to Explore Your Options?

A 30-minute confidential conversation is all it takes.

About the Author

Christoph Totter is the founder of CT Acquisitions, a buy-side M&A advisory firm in Sheridan, Wyoming. He is a published researcher in lower middle market M&A on Zenodo, Academia.edu, and ORCID, and an active contributor on LinkedIn on M&A, private equity, and business sales. CT Acquisitions works directly with 100+ buyers including PE platforms, family offices, search funders, and strategic consolidators. Buyers pay our fee, never sellers. No retainer, no exclusivity, no contract until close.